Canola Market Outlook: October 31, 2022

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans – Soybeans, meal and oil are all gaining into the new week. 220 thousand MT of sunflower oil products seem to be among the vessels stuck in Ukrainian ports as Russia unilaterally suspended their participation in the Ukraine grain corridor.

We still think that the soybean market is too cheap versus the corn market. Exports and usage are very good and crush margins are at very good levels, so crush will continue to thrive.

Canola – YTD canola disappearance into week 12 of the crop year caught up to last year’s usage and amounted to 3.6 million MT compared to 3.6 million MT last year.

Canola values are historically high but, in our view, gauged by product value they are still below current market values.

Canola usage is very good. Canadian crush margins continue to be exceptional due to the high values of the oil.

We see no reason to sell January canola. It’s too cheap relative to soybeans.

Oilseed Market Backdrop

Soybeans

Current market situation:

Soybeans, meal and oil are all gaining into the new week. 220 thousand MT of sunflower oil products seem to be among the vessels stuck in Ukrainian ports as Russia unilaterally suspended their participation in the Ukraine grain corridor.

CFTC reported managed money soybean traders were 8,549 contracts more net long through October 25 to 75,411 contracts via net new buying. Commercial soybean hedgers reduced their open interest by 75,666 contracts (or 11%). That was their largest reduction in exposure since June.

US weekly export sales of soybeans of 1.03 million MT lifted the season total to 1.16 billion bu, up 5% on last year. Sales expectations ahead of the USDA report were for 800 thousand MT to 1.6 million MT. Importantly, China took 1.12 million MT of soybeans (this is higher than the total due to cancellations to other destinations). The sales to China were impressive, but there still is uncertainty to what extend China’s ‘Zero COVID Policy’ will affect food consumption and thus longer-term demand for soybeans.

In Brazil, the flat futures and volatile currency (Brazilian Real) led Brazilian farmers to hold on to their grain ahead of a tightly contested election. Seeding in Brazil is 34% complete, but there is some unease about dryness in Brazil. There is also unease in Argentina, where farmers should start seeding in mid-November.

Soybean oil values remain quite strong, and crush margins are at record levels.

Market outlook:

With US export demand holding up and domestic crush margins at historic levels, it's tough to get overly bearish on soybeans until the South America crop is definitely made.

We still think that the soybean market is too cheap versus the corn market. Exports and usage are very good and crush margins are at very good levels, so crush will continue to thrive. We expect soybean prices to improve against corn.

Canola Market

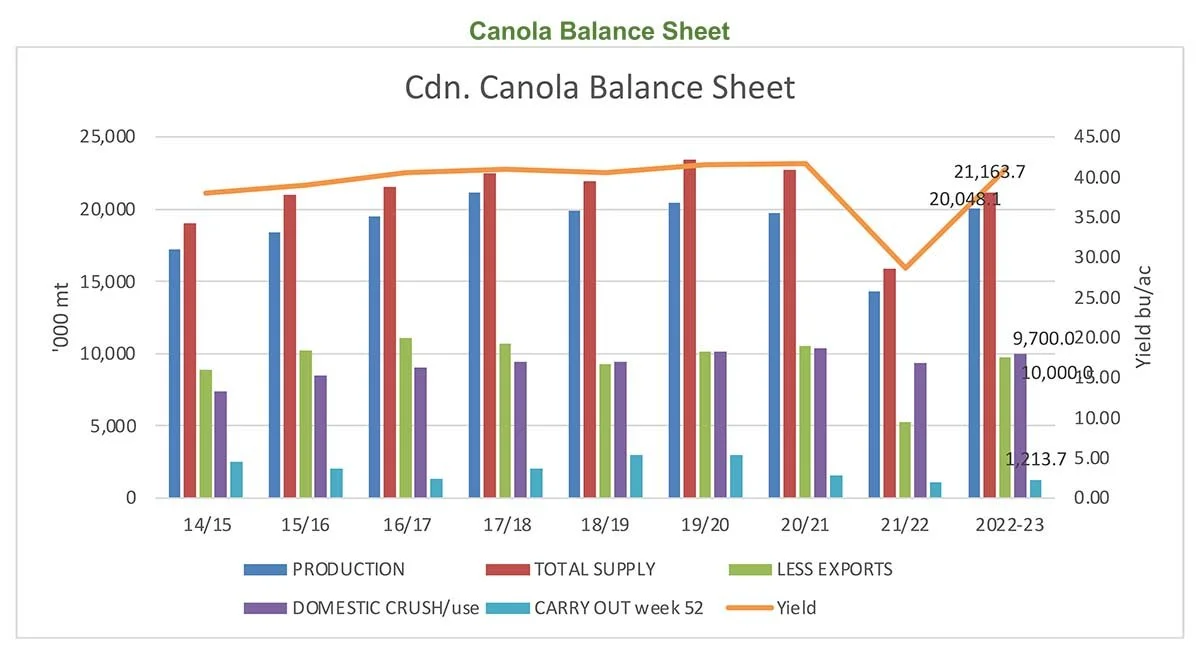

Canola usage: The Canadian Grain Commission reported that during week 12 of the crop year, growers delivered a reduced 496 thousand MT of canola into primary elevators, exports were a very good 332 thousand MT, while the domestic disappearance was also impressive at 209 thousand MT.

YTD canola disappearance into week 12 of the crop year caught up to last year’s usage and amounted to 3.6 million MT compared to 3.6 million MT last year.

Visible stocks fell slightly to 1.3 million MT, with a big 857 thousand MT in primary elevators, 181 thousand MT in process elevators, 185 thousand MT in Vancouver/ Prince Rupert, and 125 thousand MT in eastern ports.

Current market situation:

Canadian crush margins are excellent and the major companies that own export terminals and crush plants are trying to keep the canola price down to create excellent margins. Growers are selling because these are unusual prices even though, in our view, they are below current market values.

We think the best bids are from companies like P&H who do not own crush plants and by G3, who have big new export facilities in Vancouver. Unfortunately, the supply of railcars is less than what companies want to move, which keeps the basis too wide. (Rail companies supplied 81% of the ordered cars during week 11).

On a product return basis (oil and meal), canola should be at about $1.26 premium over soybeans. Soybeans in the PNW are worth at least $2.10 over futures, which equates to canola being worth about $1,000.00/MT Fob Vancouver. That is why we saw November futures rally to $950.00/MT last week and exports are so good. This should continue while the markets run at maximum crush capacity and are still short the products. Margins in China are also excellent.

In Europe, November Matif rapeseed was higher but very volatile ahead of Monday's expiry, and Canadian canola traded in a C$85 range last week. Both Matif and ICE canola are up this Monday following the suspension of the Ukraine grain corridor by Russia. (220 thousand MT of sunflower oil products seem to be among the vessels stuck in Ukrainian ports).

Market outlook:

Canola usage is very good. Canadian crush margins continue to be exceptional due to the high values of the oil. Canola is also attractive in exports markets – thanks to the high oil content in canola.

Action:

We see no reason to sell January canola. It’s too cheap relative to soybeans.

Canola – Topics of Interest

International Grains Council (IGC) on Cdn. Canola:

Following the drought year in 2021, with a record low Canadian canola production, the IGC is positive about Canadian rapeseed supply in 2022.

Even though planted area for rapeseed was lowered by 4% to 8.7 million hectares, the crop will likely be significantly larger thanks to significantly better growing conditions. This year’s canola crop is expected by ICG to reach 19.1 million MT, which compares to 13.8 million MT in the previous year. Nevertheless, the 2022 canola production will probably fall 400 thousand MT and 500 thousand MT short of 2020 and 2019, respectively.

The IGC is projecting domestic canola consumption at 10.5 million MT and exports at 8.5 million MT. In this scenario, ending stocks are projected to fall to a low 900 thousand MT.