Canola Market Outlook: November 7, 2022

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans – Weekly US soybean export sales came in at the low end of trade guesses with 830 thousand MT sold, but still CBOT soybeans made their highest weekly close in 10 weeks.

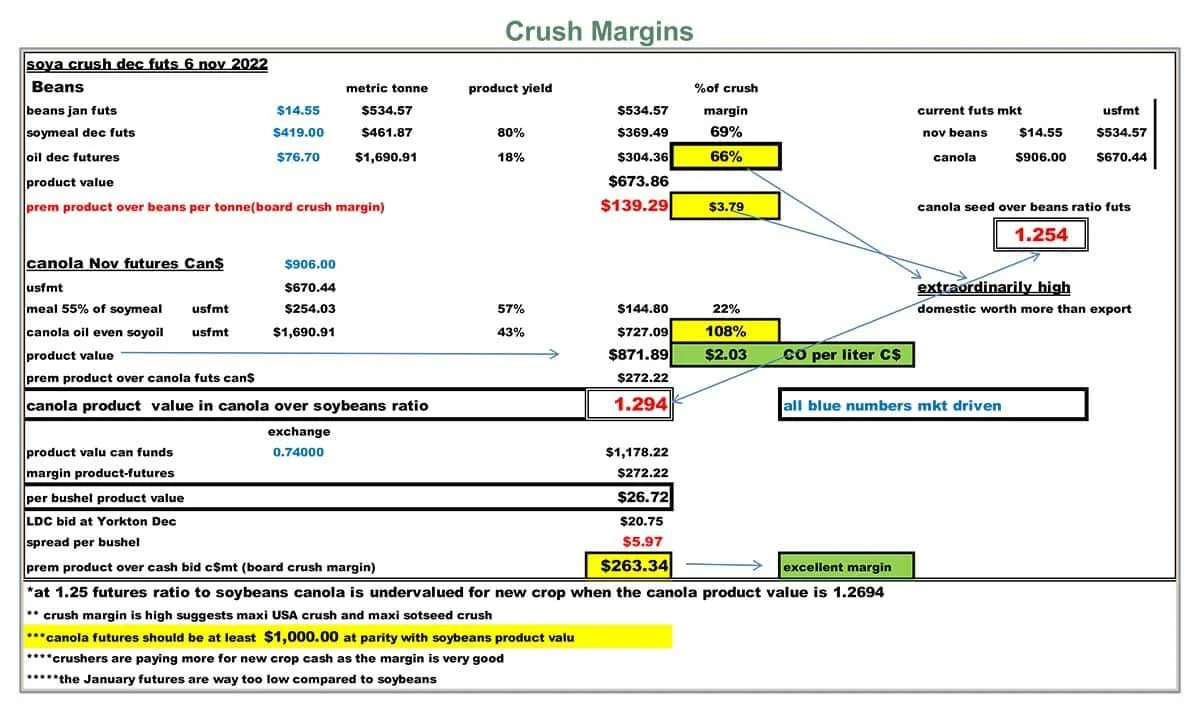

Soybean crush margins remain at record levels, and we expect to see more buying by China at these excellent margins. We will see these margins continue until at least March, when new South American crop becomes available.

Canola – Year-to-date canola disappearance into week 13 of the crop year caught up to last year’s usage and amounted to 3.96 million MT compared to 3.94 million MT last year.

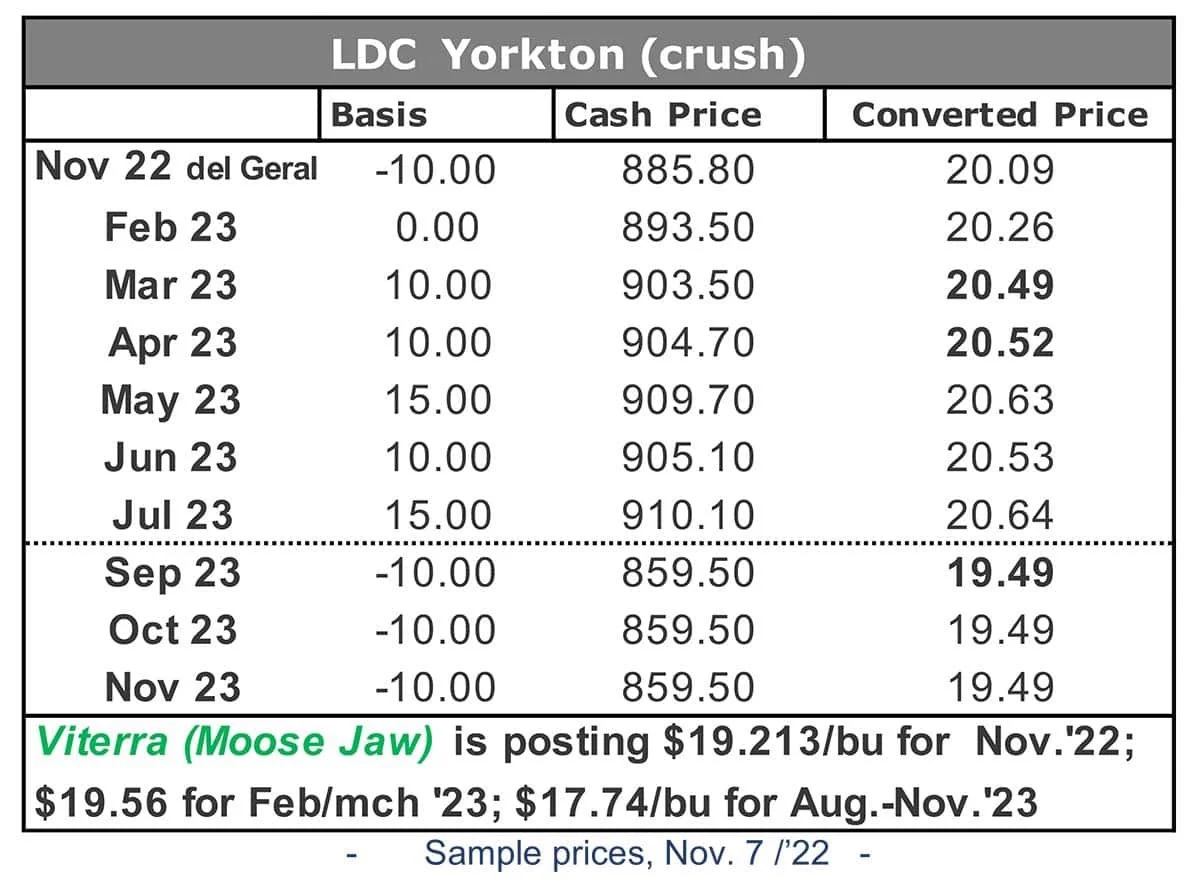

We understand that $21.25/bu has been paid in Saskatchewan against a grain pricing order.

Canadian crush margins continue to be exceptional due to the high values of the oil.

We see no reason to sell additional canola at present; we would be looking for at least $21.75 per bushel.

Oilseed Market Backdrop

Soybeans

Current market situation:

Weekly US soybean export sales came in at the low end of trade guesses with 830 thousand MT sold, which left the season total at 1,187 million bu, up just 1% on last year (up 5% last week) against the USDA's projected 5% decline. However, despite somewhat disappointing export sales and the rapid US harvest pace (88% complete versus 78% both last year and on average), CBOT soybeans made their highest weekly close in 10 weeks. Soybean oil also reached a contract high weekly close as crude oil spiked 5% and US renewable fuel production capacity rose to well over double the level of last year.

In South America, weather remains the prime focus. Brazil is expected to stay dry through next weekend, which should allow soybean plantings to approach completion. The wetter 10 to 15-day forecast should allow for good germination/ early development. Argentina looks dry through next weekend, although there is some rain in the 10 to 15-day forecast. Buenos Aires Grain Exchange (BAGE) put plantings in Argentina's core regions at just 5% complete compared to 50% a year ago.

Asian markets were also firm with palm oil up 9% at 2-month highs.

Market outlook:

The USDA report on Wednesday will be the short-term driver. The US exports pace is likely to fade going forward, and sustained rallies from here will require a South American weather problem. However, the charts are supportive. We also saw the soybean-corn ratio improve to 2.14, although it remains below where we think it should be. Soybean crush margins remain at record levels, and we expect to see more buying by China at these excellent margins. We will see these margins continue until at least March, when new South American crop becomes available.

Canola Market

Canola usage: The Canadian Grain Commission reported that during week 13 of the crop year, growers delivered 417 thousand MT of canola into primary elevators, exports were at 130 thousand MT, while the domestic disappearance amounted to a steady 215 thousand MT.

Year-to-date canola disappearance into week 13 of the crop year caught up to last year’s usage and amounted to 3.96 million MT compared to 3.94 million MT last year.

Visible stocks remained at 1.35 million MT, with a big 821 thousand MT in primary elevators, 184 thousand MT in process elevators, 215 thousand MT in Vancouver/ Prince Rupert, and 132 thousand MT in eastern ports.

Current market situation:

There has been a lot of strength in soft seed oilseeds, and crushers are enjoying record margins. Canadian elevator companies are keeping the bids lower than export values to maintain the margins in the crush plants they also own. In our view, another tightly controlled Canadian oligopoly.

We have been told that $21.25/bu was paid in Saskatchewan against a grain pricing order. To understand these prices it is important to realize that, presently, the vegetable oil share in soybeans is worth about 70% of the value of soybeans, whereas the oil yield represents only 18% in the whole seed. In canola, the oil yield is 44%, and to many customers/ users the oil is either even or has a premium to soybean oil. This means that the oil crushed in canola is worth more than the whole seed. In other words, the meal is free. Japan, China, Mexico will be crushing soft seeds, like canola, to their maximum ability.

Market outlook:

Canola is attractive in exports markets thanks to its relatively high oil content. Crush margins remain high and we expect this to support Chinese buying, especially for soft oilseeds.

Action:

We see no reason to sell additional canola at present. We would be looking for at least $21.75 per bushel.

Canola – Topics of Interest

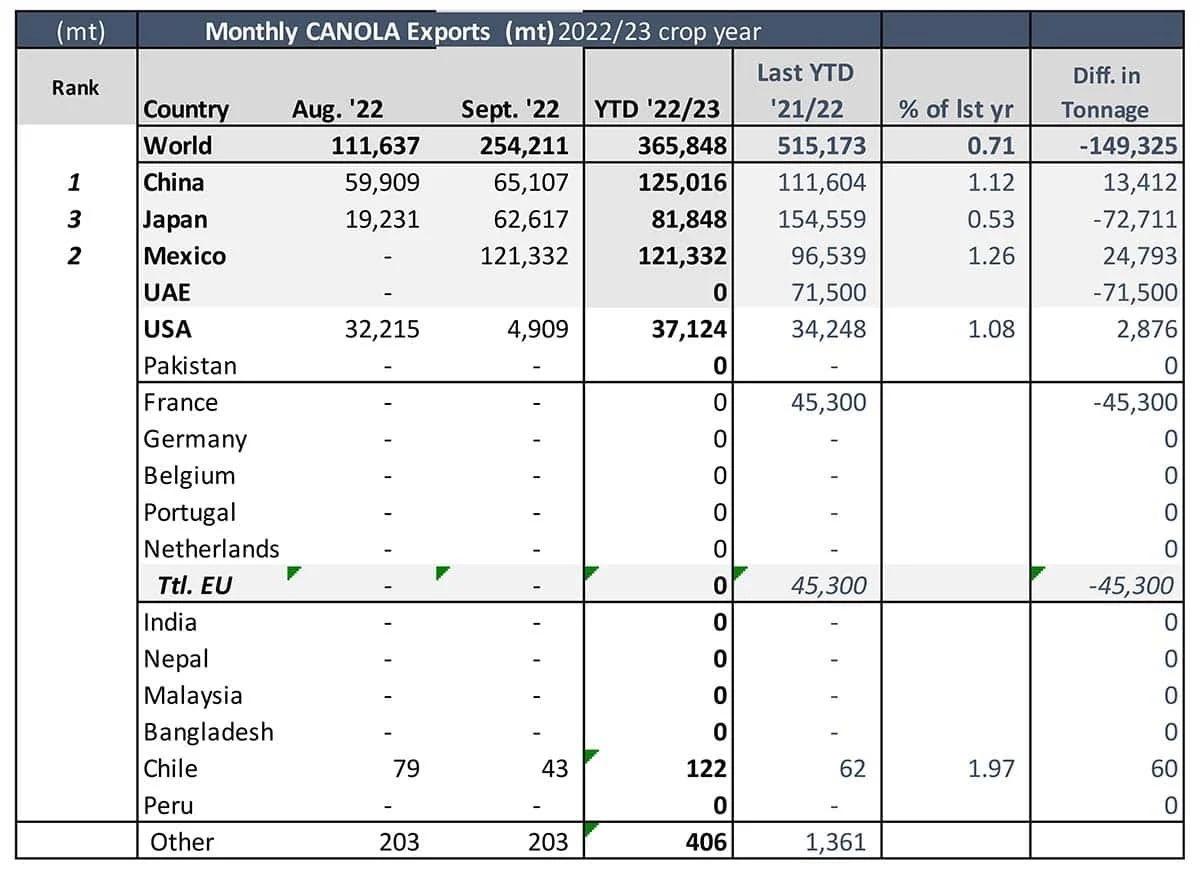

Monthly Canola Exports by Destination:

Statistics Canada (STC) published the September export data last week. Canada exported 254 thousand MT of canola during September, and 366 thousand MT of canola crop year-to-date (Aug.-Sept. 2022). Despite the bigger canola crop this year (production is up by 39% and supply by 28% over last year’s), the YTD export number is down 29% (-149 thousand MT) from last Aug.-Sept. This can partially be explained by the late harvest and slow start to shipments but is also due to an unusually high share of producer sales being allocated to domestic crush.

China has been Canada’s biggest buyer to date (125 thousand MT), followed by Mexico (121 thousand MT) and Japan (82 thousand MT). We expect total crop year exports to reach 9.7 million MT this year.