Canola Market Outlook: October 11, 2022

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans – The early support in futures came from the wheat rally and improved Mississippi River logistics, but farmers seem to be willing to sell $14/bu soybeans during harvest and this took prices off the highs.

The corn soybean ratio has dropped below 2, which we think is far too low and will correct after the crops are harvested.

Canola – Year-to-date canola disappearance into week 9 of the crop year amounted to 2 million MT compared to 2.3 million MT last year.

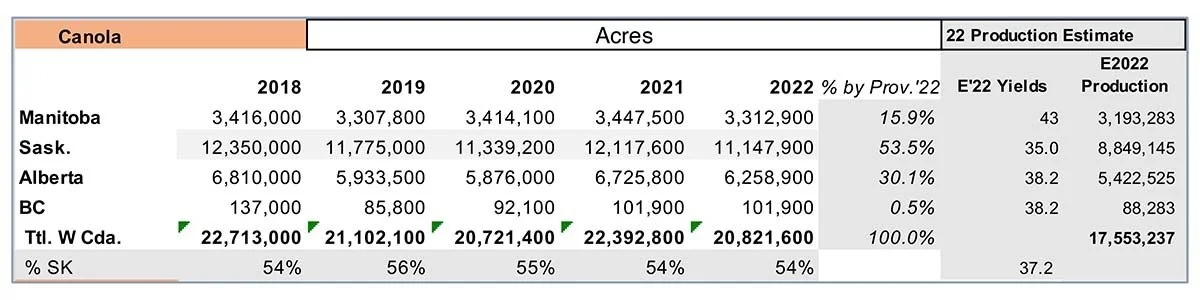

Provincial canola yield estimates continue to be lower than the StatsCan/ AAFC number.

We see no reason to sell canola right now, especially while the soybean/corn ratio is so low.

Oilseed Market Backdrop

Soybeans

Current market situation:

Harvest continued unhindered in the US. Canada is in a warm dry pattern, and a similar picture in Europe and the Black Sea also remains favorable for fieldwork.

CBOT soybeans closed better but 25¢ off the session highs, meal made a near 2-week high intra-day close, but soybean oil again failed at overhead resistance at 68¢ and closed 160 points off the session highs. The early support came from the wheat rally and improved Mississippi River logistics, but farmers seem to be willing to sell $14/bu soybeans during harvest and this took prices off the highs.

In Brazil, farmers are estimated to have planted around 10% of projected acres and have sold 19% of the 2023 crop. This is below both the 28% that had been sold a year ago and the 5-year average of 30%. Farmers have plenty of cash and some are reportedly concerned about a possible La Niña impact.

Argentina was on holiday again and farmer sales of soybeans were not updated last week. This leaves a large discrepancy between the last official data of 7.4 million MT sold during September ('Soy Peso' month), against trade estimates of close to 14 million MT sold.

Market outlook:

Export inspections and the weekly US crop update will be released later today following Monday's Columbus Day. The focus is now turning to the USDA report on Wednesday, with average trade guesses expecting little change to the US yield (current USDA estimate is 50.5 bu/acre). Beginning stocks will be raised by 34 million bu from the September stocks report, but 2022/23 exports are the subject of some debate. Current sales are 9% ahead of last year’s versus the USDA's current projected 3% decline.

Funds seem to have forgotten oilseeds as they rush to follow grains. The corn soybean ratio has dropped below 2, which we think is far too low and will correct after the crops are harvested. We expect nearby price action to be determined by tomorrow's USDA report, and then it will be down to the ratio, South American weather and Chinese demand.

Canola Market

Canola usage: The Canadian Grain Commission reported that during week 9 of the crop year, growers delivered 688 thousand MT of canola into primary elevators, exports were again a much improved 301 thousand MT, while the domestic disappearance was at 190 thousand MT.

Year-to-date canola disappearance into week 9 of the crop year amounted to 2 million MT compared to 2.3 million MT last year.

Visible stocks increased to 1.2 million MT, with a big 933 thousand MT in primary elevators, 157 thousand MT in process elevators, 109 thousand MT in Vancouver/Prince Rupert, and 39 thousand MT in eastern ports.

Current market situation:

Saskatchewan Ag reports that 82% of SK canola was harvested as of October 3, Alberta Ag shows 92% harvested, while Manitoba Ag indicates that just 58% of MB canola has been harvested. Yield assessments remained mostly unchanged, with the average SK yield shown at 35 bu/acre (up 1 bu/acre from last week), Alberta yields at 38.2 bu/acre (down 0.6 bu/acre from previously), and Manitoba yields at 35-45 bu/acre (variable by area). These provincial numbers, if correct, would imply a small crop of only ~17.6 million MT compared to 19.1 million MT in the latest AAFC report.

Grower deliveries at 688 thousand MT last week reflect good harvest progress, and exports were decent for the first time in a while. However, we worry a great deal about our ability to move the current crop by rail when markets are open for sales. Indeed, rail performance worsened last week. In week 8, CP only supplied 61% of the cars ordered and CN provided 83% of cars ordered. The railroads are moving other materials like coal, which is contrary to Canada’s global warming position, but more convenient and profitable for its shareholders than grain movement.

In Europe, Matif rapeseed bounced to a 1-week high and a second straight close above both the 20- and 50-day moving averages. Canada was closed on Monday due to Canadian Thanksgiving but is trading lower on yesterdays and today’s weakness in CBOT soybean oil.

Market outlook:

We should be hearing of more complaints to encourage the government to take some action for Western Canada on the rail front. Crush margins remain good and the corn soybean ratio below 2 is far too low and will correct after the crops are harvested.

Action:

We see no reason to sell canola, especially when the corn soybean ratio is so low.

Canola – Topics of Interest

International Grains Council (IGC):

In its latest report, IGC adjusted its estimate of 2022/23 global soybean supply down by 2 million MT to 387 million MT. Nevertheless, supply in the current crop year is likely to reach a record high, surpassing the previous year's level by just less than 1%.

The main reason for the adjustment was lower US crop expectations. US soybean production is projected at around 119.2 million MT, 4.1 million MT lower than previous expectations. Poor growing conditions have recently reduced the yield potential considerably. By contrast, the estimate for Brazilian soybean supply was raised to 146 million MT, up about 1 million MT from the previous month's forecast. The increase is mainly based on a 3% expansion in area. Ukraine is also expected to harvest more soybeans this year – 3.6 million MT, which would be up 0.7 million MT.

Global soybean consumption is currently estimated at 378 million MT, down 1 million MT on the August outlook, but 4.3% higher than 2021/22. Demand is expected to see a sharp increase, especially in China, but equally in Bangladesh and Pakistan.

In view of the bumper soybean crop, 2022/23 ending stocks are also likely to grow. 2022/23 ending stocks will increase to around 53 million MT, which is 1 million MT more than forecast in August. This translates to a 19.3% increase on last year. Ending stocks of the key exporters are expected to increase 19.5% year-on-year. US soybean stocks are assumed to shrink for the fourth season running, dropping to 4.6 million MT, the lowest level in 13 years.