Canola Market Outlook: August 2, 2022

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans – Last week, CBOT August soybeans rose by over $2/bu with November up $1.10 at a six-week high close. However, CBOT soybeans fell sharply to start the new week yesterday and ended near the lows with a huge 85¢/bu trading range.

Surprise weekend rains and a 5% reversal in crude oil pressured the market, but it was the concern over the impact on Chinese demand for US soybeans, with a visit to Taiwan by Nancy Pelosi, which provided the biggest strain.

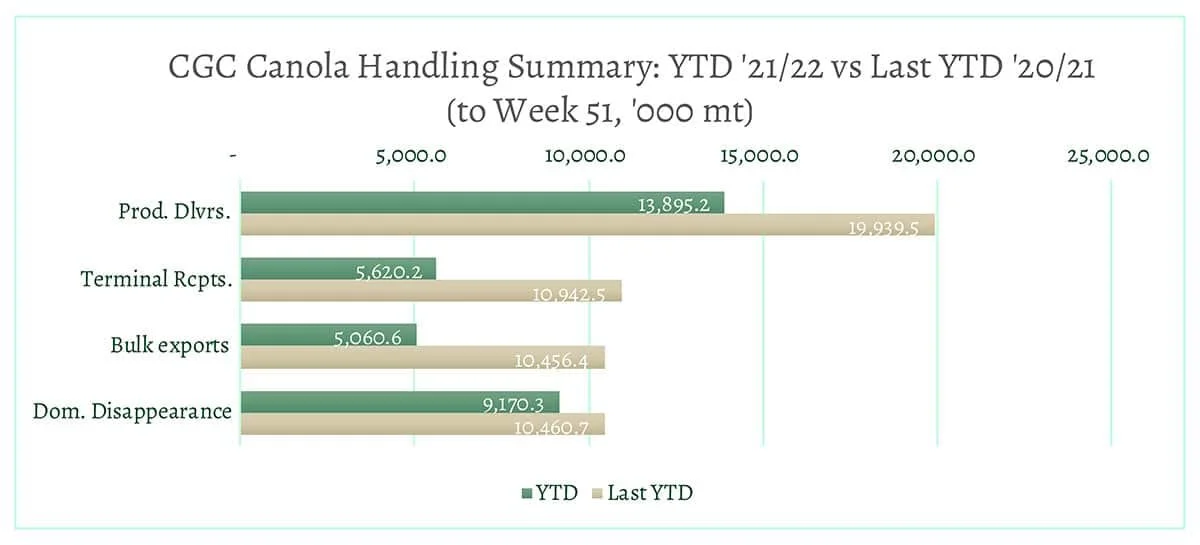

Canola – Total canola disappearance during the 51 weeks of the crop year amounted to 14.2 million MT compared to 20.9 million MT last YTD.

The losses in oil value over the past two days are a drag on oil-rich canola. However, ending stocks in Canada are very low and we expect growers will get very good prices for early deliveries. We would hold additional sale for now.

Oilseed Market Backdrop

Soybeans

Current market situation:

Last week, CBOT August soybeans rose by over $2/bu with November up $1.10 at a six-week high close. Good/Excellent ratings for the US fell 2% to 59% – only 26% were setting pods with the return of heat and dryness forecast, plus export sales for 2022/23 sit at an 8-year high. However, CBOT soybeans fell sharply to start the new week yesterday and ended near the lows with a huge 85¢/bu trading range. Surprise weekend rains were the early catalyst for the change, and a slightly improved crop report yesterday. (The weekly crop update raised ratings 1% to 60% Good/Excellent, in line with last year. Crop progress was mixed with 79% blooming and in line with the average, but just 44% is setting pods against the five-year average of 51%). This was followed by a 5% reversal in crude oil, but it was the concern over the impact on Chinese demand for US soybeans, with a visit to Taiwan by Nancy Pelosi, which provided the biggest strain.

Farmer selling in Brazil was negligible following the CBOT plunge. Brazilian FOB offers were largely pulled with crushers paying better levels than the export market. The August line-up shows 4.8 million MT to be loaded, with the final July load-out at 7.25 million MT. Brazil's Agriculture Minister said Chinese authorizations for Brazilian soymeal imports may be granted within two months. However, China imports no more than 50,000 MT of soybean meal annually, so this seems irrelevant.

Market outlook:

The market will be almost totally focused on US weather for several weeks yet, with the August USDA report due in 10 days’ time.

Basis the USDA's current demand, the loss of just 1 bushel per acre of yield would send stocks below 150 million bushels which would send soybeans into rationing mode.

Canola Market

Canola usage: The Canadian Grain Commission reported that during week 51 of the crop year, growers delivered 155 thousand MT of canola into primary elevators, exports were 29 thousand MT, while the domestic disappearance was at 177 thousand MT. Crush volume still averages at 180 thousand MT per week. Exports are running at 99 thousand MT per week (5.16 million MT annualized).

Total canola disappearance during the 51 weeks of the crop year amounted to 14.2 million MT compared to 20.9 million MT last YTD.

Visible stocks fell to 641 thousand MT, with 162 thousand MT in process elevators, 89 thousand MT in Vancouver/ Prince Rupert, and 66 thousand MT in eastern ports.

Year-to-date usage (export and crush) at 14.2 million MT is 32% smaller than last YTD.

Current market situation:

Soybean oil rallied nicely last week, which improved canola prices. Crush margins are very good, so we expect growers will get very good prices for early deliveries. However, this week surprise weekend rains in the US, weak crude oil values, and geopolitics in the form of Nancy Pelosi’s visit to Taiwan (which China disapproves of) caused a reversal in oilseeds.

Matif rapeseed in Europe followed the CBOT with a close to 6% decline. Canada was closed on Monday but is getting hit hard overnight and today with a ~C$50/MT (~4.5%) decline. Asian markets are also all trading sharply lower this morning following yesterday's slump at the CBOT, the reversal in crude/energy, and another distorting move on exports by the Indonesian GvMT. This cut the export tax reference price and raised exportable volumes. Palm oil is down over 5% today and 11% on the week. The losses in oil value are a drag on oil-rich canola.

Regarding Canada, we need to reduce our export projection for the outgoing year but will do so next week after we see the numbers for week 52.

Market outlook:

Following Nancy Pelosi’s visit to Asia, we expect the attention of the oilseed markets to return to US weather as we move into August. The forecast looks hot and dry to start. Given the USDA's current demand numbers, the loss of just 1 bu/acre of yield would send stocks below 150 million bu and into rationing mode. Current crop ratings and the current two-week forecast argue that making the USDA’s 51.5 bu/acre yield may be a tough ask.

Action:

We expect growers to get very good prices for early deliveries. We would hold additional sale for now.

Canola – Topics of Interest

Latest Canola Crush Statistics:

The StatsCan June crush numbers for Canada showed 660 thousand MT for the month, compared to 830 thousand MT last crop year, and 865 thousand MT for 2019/20. However, the June crush was 68 thousand MT bigger than the May 2022 crush.

The year-to-date crush (August 2021 to June 2022) adds to 7.9 million MT compared to 9.6 million MT last year-to-date, a 19% reduction in volume. Annualizing the YTD crush yields 8.5 million MT for the ongoing crop year.