Canola Market Outlook: July 25, 2022

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans – The CBOT soybean complex ended last week lower across the board, and new crop soybeans are now very close to the 2022 lows set back in January.

However, crop ratings dipped to their lowest of the season, and the USA making its first sale to China for the first time in 7 weeks, but there is some concern about long-term demand from China because of its extensive COVID lockdowns.

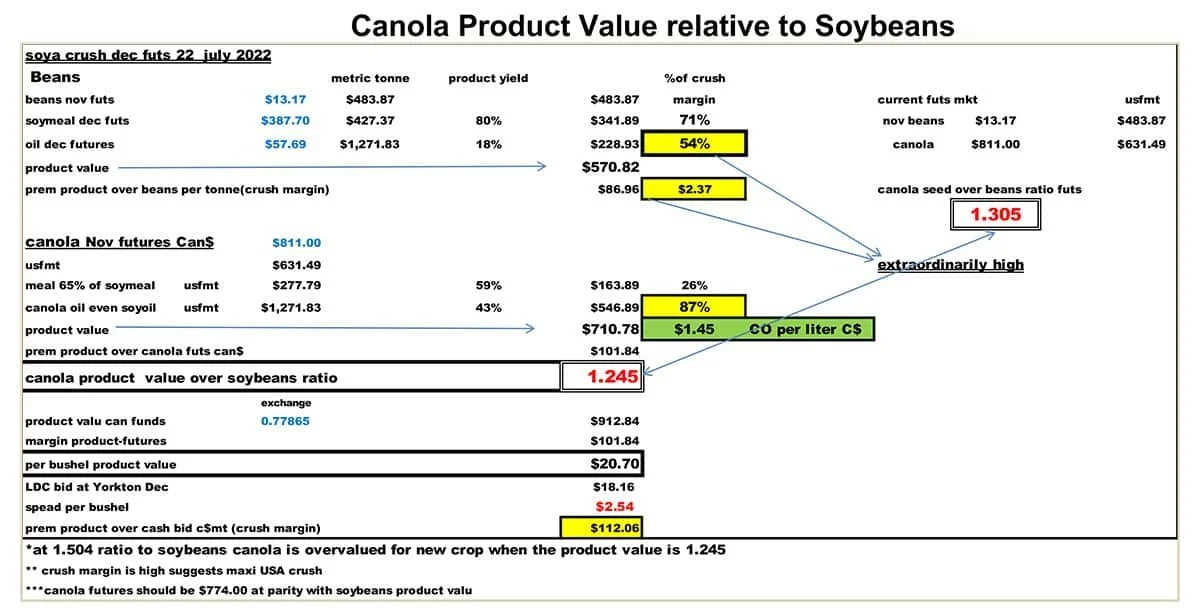

Canola – Total canola disappearance during the 50 weeks of the crop year amounted to 14 million MT compared to 20.5 million MT last year-to-date.

Given our earlier sales, we would not sell additional canola for the time being as the crop is late and weather still is a major factor.

Oilseed Market Backdrop

Soybeans

Current market situation:

The CBOT soybean complex ended last week lower across the board, and new crop soybeans are now very close to the 2022 lows set back in January.

Nevertheless, nearby board crush margins rose another 10¢ to $1.82, new crop margins are above $1.60 and cash margins are even higher. This will keep domestic demand for soybeans elevated, while the bulls will have been pleased to see some old crop export sales.

Other news was limited, although crude/energy prices saw another sharp reversal while the US dollar was weaker. Market attention will increasingly turn to August weather this week onward.

Turning to Brazil, the Real dropped to 6-month lows, but this was not enough to offset the losses at the CBOT, so country movement was slow. However, the slide in the Brazilian Real since May almost exactly matches the drop in CBOT soybeans over the same period, so that Brazilian farmers are still receiving unchanged prices in local currency (while US farmers are getting much lower prices).

Currency also is a major factor for Argentine farmers. The official rate of the Argentine peso against the US dollar is around 133, while the parallel ‘blue rate’ (informal rate) is now over 330.

Market outlook:

CBOT soybeans made their lowest weekly close since January. This, despite:

export sales being positive for the first time in 4 weeks,

the US making its first sale to China for the first time in 7 weeks, and

crop ratings dipped to their lowest of the season.

The soybean/corn ratio also dropped. We can only say this makes little sense to us and soybeans simply followed the other markets downwards.

We see no reason to sell soybean products and prefer to watch the weather for the present. Chart-wise, November looks oversold.

Canola Market

Canola usage: The Canadian Grain Commission reported that during week 50 of the crop year, growers delivered 193 thousand MT of canola into primary elevators, exports were 11 thousand MT, while the domestic disappearance was at 213 thousand MT. Crush volume still averages at 180 thousand MT per week. Exports are running at 101 thousand MT per week (5.2 million MT annualized).

Total canola disappearance during the 50 weeks of the crop year amounted to 14 million MT compared to 20.5 million MT last YTD.

Visible stocks fell to 695 thousand MT, with 171 thousand MT in process elevators, 80 thousand MT in Vancouver/ Prince Rupert, and 73 thousand MT in eastern ports.

Year-to-date usage (export and crush) at 14 million MT is 32% smaller than last YTD.

Current market situation:

It has become pretty clear now that we had bigger supplies of canola than our government statisticians thought by quite a long way. We expect at least 300,000 MT more will be delivered by the end of the crop year. The visible is under 700,000 MT at 695,000 MT. We expect to find the first six weeks of the new season to be the tightest.

For new crop, crop ratings have been fairly good, with Saskatchewan Agriculture last rating canola at 68% in Good to Excellent condition, and Alberta Agriculture rating canola at 68% Good to Excellent. Recent rains will have further improved conditions.

In Europe, Matif rapeseed remains extremely volatile, closing down at €6 last week, but still €23/MT off the session lows. It equalled the 2022 lows set back last January.

Asian vegetable oil markets ended higher. Indonesia delayed the implementation of its B35 bio-diesel plan and may scrap its domestic sales policy (because of the high inventories that the policy has created), while Malaysia said it was losing the equivalent of 1.5 million MT of production each month due to labour shortages.

Market outlook:

Soybeans are somewhat on alert with USDA putting 26% of US soybean acres into drought territory. On the other hand, demand from China carries an increasingly big question mark because of the severity of the impact on the economy of President Xi's Zero-COVID policy. The policy now has 250 million people under full or partial lockdown (17.5% of the economy).

The losses in oil value in oilseeds are weighing on canola, although Asian vegetable oil markets did end the week higher due to potential changes in Indonesian domestic policies.

Action:

We would not sell additional canola for the time being as the crop is late and weather still is a major factor.

Canola – Topics of Interest

For 2021/22, Australia has become the primary rapeseed supplier of the European Union

The EU-27 imported 5.3 million MT of rapeseed from outside the EU during the 2021/22 season, just ½ million MT short of 2020/21 imports. Domestic EU rapeseed supplies (production plus carry-in) was ~1.2 million MT smaller than in 2020/21.

Rapeseed/ canola imports from Canada at 611 thousand MT were down 71% from the previous year. Imports from the Ukraine at 1.7 million MT were down 24%, partly as a result of the Russian invasion of the Ukraine.

In contrast, rapeseed shipments from Australia to the EU increased to 2.9 million MT, up 48% from the year prior. Accordingly, the Australian market share increased by 19% to 53%.