Canola Market Outlook: May 27, 2024

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans: The soy complex had a mixed week. CBOT soybeans and meal made gains, while oil was weaker going into the three-day holiday.

The USA soybean planting pace is slow at 52% planted, but new crop exports sales remain very slow and are at multi-season lows.

We have seen the premium for soybeans planting over corn reduce, but we expect it to reduce further. We see more demand in Europe for feed grains than for protein.

Canola: YTD total canola disappearance into week 42 of the crop year amounts to 14.3 million MT compared to 15.3 million MT last year and is down 7% on last year.

Seeding progress in Cda. has fallen well behind normal, but soil moisture has improved significantly over the past month.

ICE canola remains torn between the bullishness in rapeseed in the EU (new crop Matif rapeseed has traded above €500/mt), and the lacklustre soybean oil market in the USA.

We would leave canola alone while there are problems in the EU.

Oilseed Market Backdrop

Soybeans

Current market situation

The soy complex had a mixed week. CBOT soybeans and meal made gains (July soybeans were up 20c /bu on the week, Nov. soybeans +16c; meal was up 18c on the week), while oil was weaker going into the three-day holiday(-32c).

The weekly Commitment of Traders data showed spec funds in soybean futures and options cutting back by another 16k contracts from their net short position to a net short 26,426 contracts. Commercials saw an increase to their net short by 20k contracts to -65,706 contracts.

USDA export sales data has the total export commitments for old crop soybeans at 42.9 million mt, which is 93% of USDA’s export forecast, 6% behind the average pace. Total sales for new crop soybeans have totaled just 955,887 mt, down 49.7% from a year ago, as China has yet to be in for any new crop.

The USA soybean planting pace is slow at 52% planted, 9 points behind last year’s pace, wet weather is slowing the campaign. Meanwhile, new crop exports sales remain very slow and are at multi-season lows.

In Brazil, the Rio Grande do Sul (RGDS) flood damage continues to be assessed. Loss assessments range from 2 to 3.5 million mt. This helped support local crush margins and soybean oil premiums which rose to option price against CBOT. In Argentina, BAGE kept their 50.5 million mt Argentine crop number. Harvest there is now 78% complete.

Market outlook

The outlook is a mixed bag: The European oilseed complex is the best supported region thanks to very difficult weather conditions this spring. In the US, nearby cash shorts are keeping meal supported, and in South America products are supported by the flooding complications/ outages in RGDS. We do not think that slow seeding progress in the US is too worrying so far, plus the US has barely sold any new crop soybeans.

We have seen the premium for soybeans planting over corn reduce, but we expect it to reduce further. We see more demand in Europe for feed grains than for protein.

Canola Market

Canola usage

During week 42 of the crop year, growers delivered 255 thousand MT of canola into primary elevators, exports were 106 thousand MT, while domestic disappearance amounted to 231 thousand MT.

YTD total canola disappearance into week 42 of the crop year amounts to 14.3 million MT compared to 15.3 million MT last year and is down 7% on last year.

Visible stocks remained to 1.09 million MT, with 495 thousand MT in primary elevators (-135k mt from last week), 153 thousand MT in process elevators (-36k mt), 190 thousand MT in Vancouver/ Prince Rupert (+47k mt), and 131 thousand MT in eastern ports.

Current market situation

Seeding in Canada has progressed despite varied shower activity, with just 20% planted in MB (as of May 21), 50% in SK (as of May 20) lagging the 5-year average by 20%, and 40% planted in AB (as of May 21). However, while seeding progress is falling well behind normal progress, soil moisture has improved significantly over the past month.

Meanwhile for the current crop year, commercials are keeping the grower bids for seed low, so that their crush plant margins are satisfied rather than making seed exports.

In Europe, new crop Matif rapeseed has traded above €500/mt while the trade assesses a very difficult spring dominated by wet weather and late frosts, replanting with spring crops, and accompanied by a lack of farmer selling. Rapeseed oil traded above the €1,000/mt benchmark and sunflower oil also extended gains above $1,000/mt.

Market outlook

Poor weather is causing delays in Europe in the planting of rapeseed and prices are much stronger. In Canada, ICE canola remains torn between the bullishness in rapeseed in the EU, and the lacklustre soybean oil market in the USA.

The visible in Canada has reduced, which suggests to us that the crop was overstated. We will have to see if the deliveries remain modest.

Action

We would leave canola alone while there are problems in the EU.

Canola – Topics of Interest

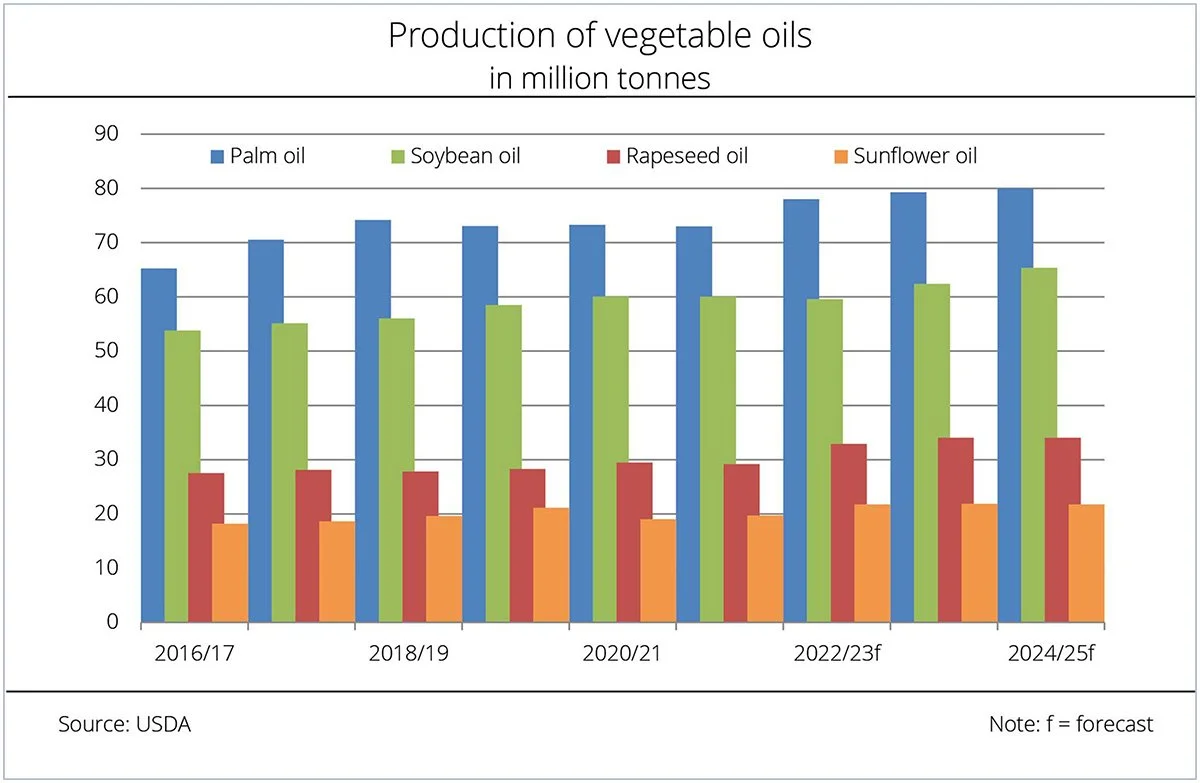

Global vegetable oil production outlook

According to USDA, the ‘24/25 global vegetable oil production will amount to 228.3 million mt. If correct, this would be a 4.5 million mt higher than production in ‘23/24. This would more than cover the demand projection of 224.9 million mt.

Within the vegetable oils, palm oil is set to remain the world's most important vegetable oil in terms of manufacture and consumption, with global output estimated at 80 million mt, a 715,000 mt increase over ‘23/24. Palm oil accounts for just over 35 per cent of total global vegetable oil production. Indonesia remains the largest producer with an output of 47.5 million mt, followed by Malaysia with 19 million mt and Thailand with just less than 3.4 million mt.

The production of soybean oil is expected to grow just less than 3 million mt to 65.4 million mt in the coming crop year and could hit a new record. China remains the primary producer with production amounting to 18.5 million mt based on large seed imports. The US ranks second with 12.9 million mt.

The production of rapeseed oil is expected to reach 34 million mt in 2024/25, slightly less than in ‘23/24. By contrast, production of sunflower seed oil is seen to drop around 103,000 tonnes to 21.7 million mt in 2024/25. This estimate reflects production declines in Argentina and Ukraine. The expected increase in sunflower oil production in the EU-27 is unlikely to offset these decreases.