Canola Market Outlook: July 24, 2023

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Markets are very strong following the closure of the Black Sea corridor, the Russian bombing of Ukrainian ports, and forecasts of more dry conditions in the USA.

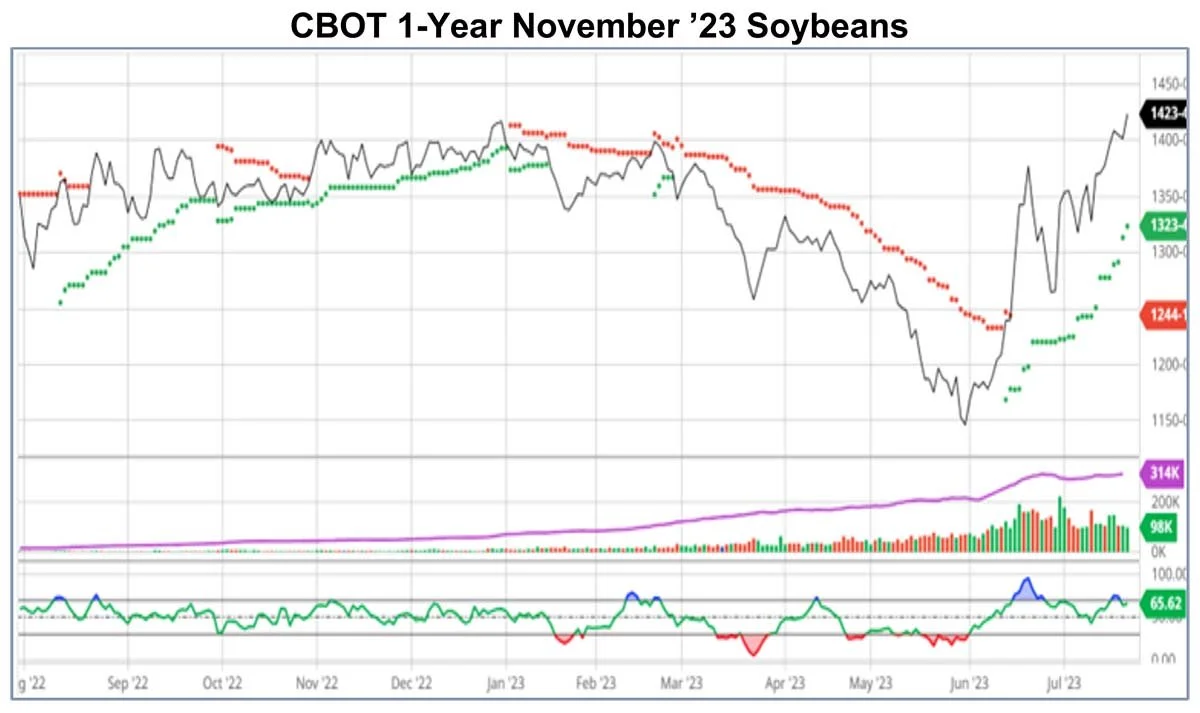

Soybeans are very strong and have gained 55 cents per bushel ($27.00 cfmt) since last week. The November contract is just 2 cents per bushel under the session high and working at the strongest quotes since last spring.

Crush margins have also gained with reports of $3.00 per bushel being paid to soybean crushers in the USA which is excellent and well above the average.

Funds are buyers of the market adding to their long.

The International Grain Council reduced their 23/24 global soybean crop estimate by 2 myn tonnes.

Abiove Brazil estimates the 23/24 Brazilian soybean crop at 156.5 myn tonnes, a slight increase from their June forecast.

The USDA reported that China purchased 121,000 tonnes of USA soybeans today which means the USA South American spread has narrowed.

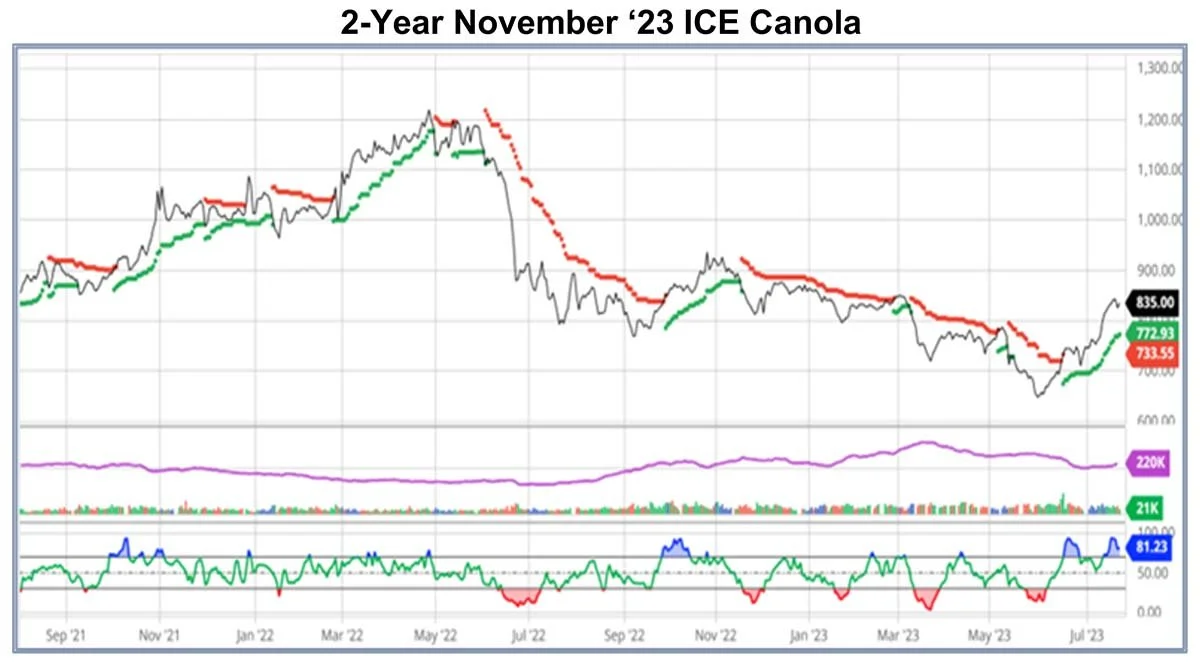

Canadian canola also strengthened following soybeans but less so.

Oilseed Market Backdrop

Soybeans

Current market situation

Weather conditions still dominate the USA futures markets with reports of record temperatures and dry conditions in much of the bean area.

Funds are buying in a thin market where growers are not sellers.

The Chinese made their first purchase of USA soybeans which suggested they were now more competitive to South American prices.

The USA Ag Attaché put the Argentine bean crop at 21.25 myn tonnes against the USDA's 25 myn tonnes, whilst the June Argentinian crush was down 21% YoY to 3.1 myn tonnes.

August weather is key to USA soybean production with current forecasts looking dry and hot.

Strength in the products continues to support crush margins with nearby crush margins reported above $3.00 per bushel.

Market outlook

The futures markets will continue to respond to weather conditions in the USA.

Canola Market

Canola usage

In week 50, growers delivered 396,000 tonnes, exports were only 94,000 tonnes, and domestic usage was said to be a strong 217,000 tonnes. In our view, StatsCan underestimated the crop supply, and we will see by how much from the first six weeks of the new crop year delivery period. It will be old crop stocks for at least the first 6 weeks. The low export number was more from lack of demand at the Canadian offered prices than supplies. Exporters who also own crush plants retained seeds to earn very good crush margins.

Current market situation

We expect that canola prices will continue to follow USA soybean futures but to a lesser extent. Growers will not sell more new crop whilst dry conditions in Canada persist. Canadian prices are not competitive to the EU, so we must rely on Chinese buying to support the export trade.

Market outlook

The oilseeds markets will watch the weather outlooks very closely to see if drought conditions in North America are realistic whilst South American sales continue at a record pace. The markets could be very volatile. The trade was under estimating supplies in their estimate of what the WASDE report would say.

Action

Without EU demand we still think it is warranted to have a good percentage sold at current levels. Growers need to watch the weather.

Canola – Topics of Interest

Global Rapeseed Prices

Global rapeseed prices were higher in all major exporting countries last week. According to IGC data, rapeseed prices in the EU rose $49/mt over the week to $563/tonne while Canadian values were up by $38/tonne to $678/tonne. Meanwhile, prices in Australia and Ukraine only rose by $29/tonne and $15/tonne respectively. The increase in prices narrowed the spread between EU and Australian values but widened the spread between Canada and other competing origins.