Canola Market Outlook: August 15, 2022

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans – The market held its gains following the USDA report, despite a higher-than-expected yield and a record crop of 4.53 billion bu which, despite a higher export number, left 2022/23 ending stocks up 15 million bu at 245 million bu.

In our view, the corn/soybean ratio is too low given the balance sheet. We would not like to be short November soybeans here.

Canola – Total canola disappearance during week one of the crop year amounted to 151 thousand MT compared to 309 thousand MT last year.

The demand outlook remains positive for an oil-driven crop like canola. We also believe soybeans have room to appreciate, so we see no reason to sell additional canola at this time.

Oilseed Market Backdrop

Soybeans

Current market situation:

Solid demand and a weak US dollar lifted September soybeans by almost 70¢/ bu ahead of the USDA report. November was up 40¢ /bu at a 75¢ discount to the September contract.

The market held its gains following the USDA report, despite a higher-than-expected yield and a record crop of 4.53 billion bu which, despite a higher export number, left 2022/23 ending stocks up 15 million bu at 245 million bu. The small increase to a record US yield (51.9 bu/acre) and a 900 thousand MT hike in the Chinese crop were the only changes in production numbers. On the demand side, global domestic consumption was raised 500 thousand MT with a 400 thousand MT drop in the EU offset by a 750 thousand MT rise in Brazil.

CONAB in Brazil left Brazil's soybean crop unchanged at 124 million MT (USDA is at 126 million MT). The USDA also kept the 2023 crop at 149 million MT, so that total South American production is forecast to rise by 26 million MT.

In Argentina, the Rosario GE put the 2023 crop at just 47 million MT, while USDA left production unchanged at 44 million MT for 2022 and 51 million MT for 2023.

The USDA made no changes to Chinese imports, but they raised this year's production by 900,000 MT to 18.4 million MT.

Traders consider that there is still a lot of weather to get through before final US yields are conclusively determined and the crop is in the bin.

Back in the US, this morning’s National Oilseed Processors Association (NOPA) report showed that 170.2 million bu of soybeans were crushed during July. That was shy of the average trade estimate, but 9.7% larger year-over-year and the second largest for the month on record, behind 2020. Soybean oil stocks at 1.68 billion lbs were below estimates.

Market outlook:

We expect that farmer selling will be slow in South America as interest rates soar and growers retain dollar valued crops as much as they can. Chinese demand is a potential issue, with the Chinese government suggesting imports of 95 million tonnes, some 3 million tonnes below the USDA number. The corn/soybean ratio, in our view, is too low given the balance sheet. We would not like to be short November soybeans here.

Canola Market

Canola usage: The Canadian Grain Commission reported that during week one of the crop year, growers delivered 122 thousand MT of canola into primary elevators, exports were a tiny 7,000 MT, while the domestic disappearance was at 144 thousand MT.

Total canola disappearance during week one of the crop year amounted to 151 thousand MT compared to 309 thousand MT last year.

Visible stocks fell to 481 thousand MT, with 151 thousand MT in process elevators, 82 thousand MT in Vancouver/ Prince Rupert, and 18 thousand MT in eastern ports.

Current market situation:

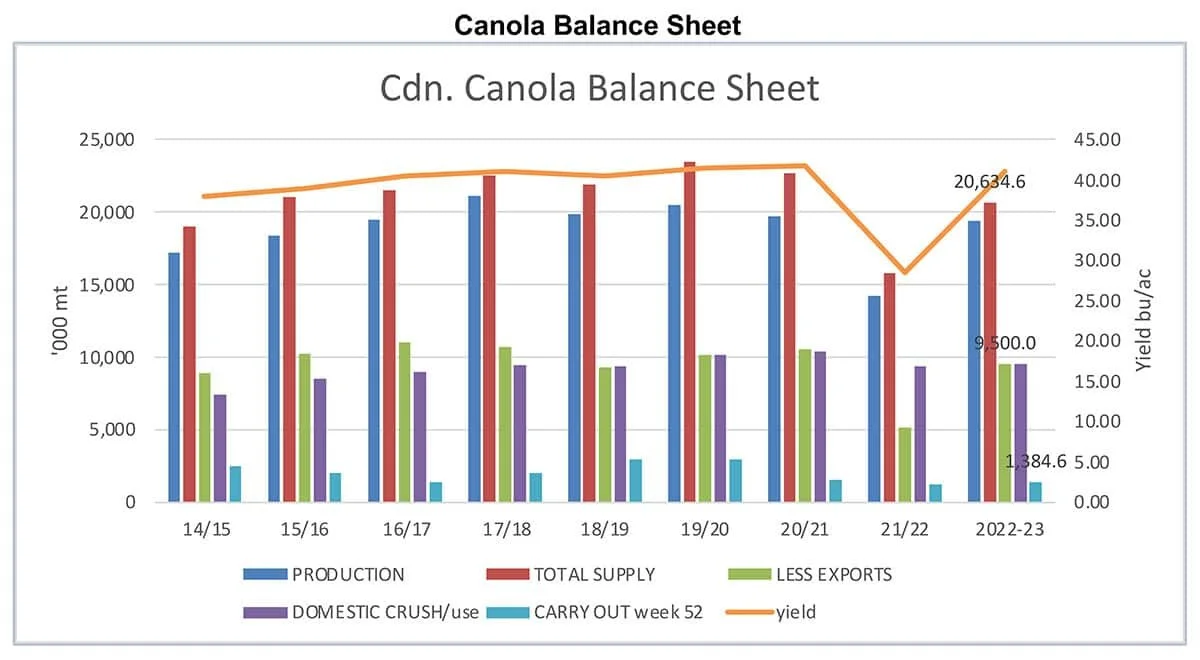

Growers delivered 122,000 MT of canola in week one of the new shipping year 2022/23. We will use the first six weeks of canola deliveries to calculate the old crop stocks on farm. Given what we can gather so far, we have adjusted to 2021/22 canola supply to 15.8 million MT, against total usage of 14.6 million MT (5.1 million MT exports and 9.3 million MT domestic use, plus some seed/ waste). This leaves us with a 2021/22 carryout number of 1.2 million MT.

For the 2022/23 crop year, we expect a supply of 20.6 million MT (19.5 million MT production plus carry-in). Yields should be much improved this year compared to last year. Alberta Agriculture is showing an estimated yields of 40.5 bu/acre, and we expect similar yields in Saskatchewan. This would again allow for exports and crush at around 9.5 million MT each. If achieved, this would result in 2022/23 ending stocks of 1.38 million MT, which is actually a similar stock-use ratio as this past crop year.

With respect to exports in the new crop year, much will depend on how much canola China will want to buy from Canada. However, China is pragmatic about commodity values, and at current valuations of the oil portion in oilseeds, canola will be the preferred commodity relative to soybeans (see graph on canola product value). We expect China to get close to the tonnages bought in 2015 and 2016. One worry is availability of railcars when needed for grain exports. We hope increased shipments of (dirty) coal will not impede exports of much needed grain.

Matif November rapeseed closed virtually unchanged Friday from the start of the week but was down this Monday. Futures remain volatile, but thinly traded.

Market outlook:

The demand outlook remains positive for an oil-driven crop like canola.

Action:

We believe soybeans have room to appreciate, so we see no reason to sell additional canola at this time.

Canola – Topics of Interest

USDA – Global rapeseed outlook:

USDA expects rapeseed production to recover to 82.5 million MT in 2022/23 from 72.3 million MT in 2021/22. Most of the rebound is based on an improved production outcome in Canada. This would re-instate Canada as the biggest producer, ahead of the EU, China and Australia.

Global trade in rapeseed is also forecast to rebound, with more demand especially from China.

Global rapeseed crush for 2022/23 is forecast at a record, with the EU as the primary processor and consumer. Canada crush is expected to recover, making more rapeseed meal and rapeseed oil available to the global market.

European Commission – Increase in EU sunflower area neutralised by poor yields

The war in Ukraine and the associated shortage of sunflower oil motivated many farmers in the EU to sow more sunflowers in the spring of 2022 (+10% acres to 4.8 million acres). However, the initially positive harvest prospects have been negatively impacted by the dryness in many parts of Europe.

The continuing drought in Europe (especially in the eastern and south-eastern regions) prompted the EU Commission to drastically lower their production outlook for sunflower seed. At the end of July, Brussels anticipated a volume of 10.5 million MT, 636,600 MT less than the previous month. This would be only 200,000 MT, or 1%, more than in 2021.

The EU Commission is currently expecting yields in the amount of only 0.218 MT per hectare, down from an average of 0.238 MT per ha.