Canola Market Outlook: July 10, 2023

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans - CBOT soybeans closed the week down 14c/bu and a full 60¢/bu off the early week highs. Soybean meal lost $11, while the oil share posted further gains with soybean oil up 0.87c/lb ($19/mt).

This week’s crop ratings report showed a slight improvement (plus 1 point to 51% Gd/Exc).

The US soybean balance sheet will be scrutinized intensely and debated for weeks to come. We do not expect any major changes in the WASDE report.

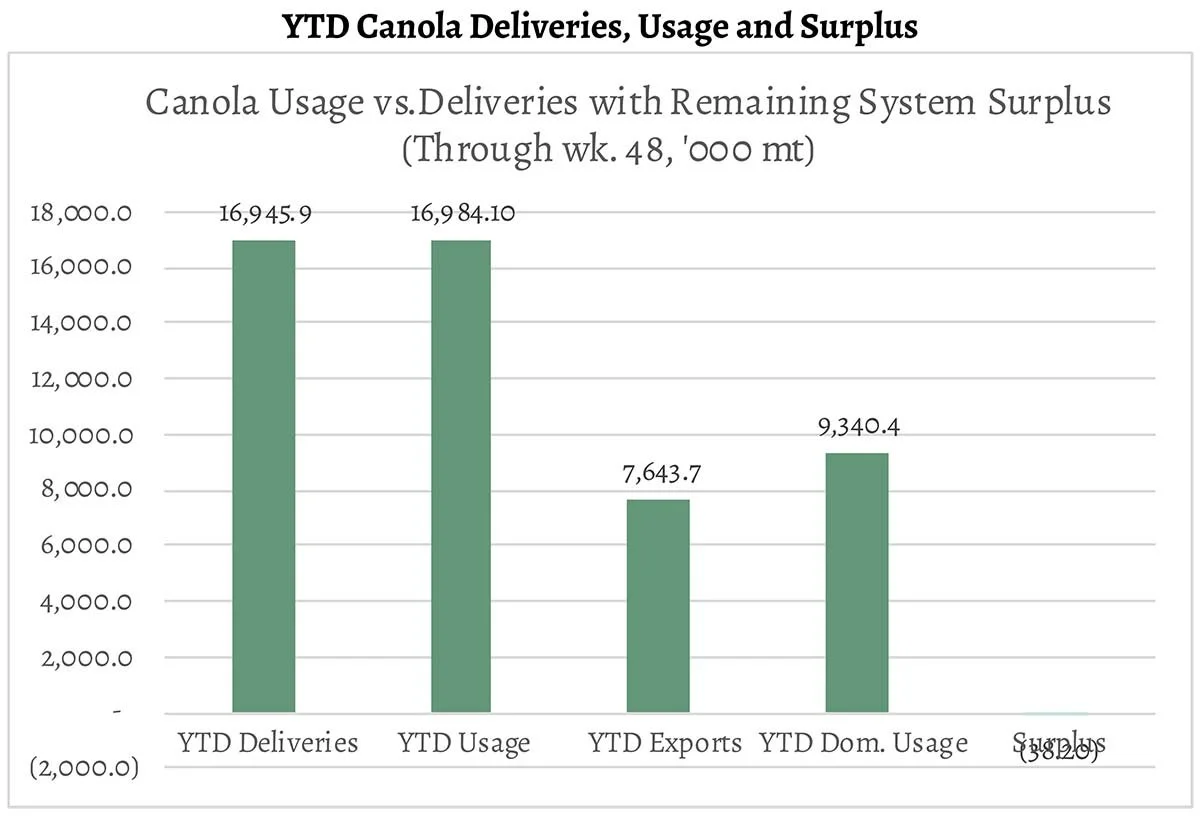

Canola - YTD canola disappearance into week 48 of the crop year is 25% above last year’s (drought-reduced) usage (+3.4 million MT) and amounted to 17 million MT compared to 13.5 million MT last year.

Canola crop ratings in SK fell by 11% from June 12th to 66% Gd/Exc on June 26th. Reports from central Alberta are also not encouraging. It is becoming questionable if average yields will be achieved unless widespread rains alleviate drought stress.

We don’t see the need to make more sales for now.

Oilseed Market Backdrop

Soybeans

Current market situation

CBOT soybeans closed the week down 14c/bu and a full 60¢/bu off the early week highs. Soybean meal lost $11, while the oil share posted further gains with soybean oil up 0.87c/lb ($19/mt).

Lat week’s US crop ratings at 50% Gd/Exc fell 1 point, but this week’s report showed a slight improvement (plus 1 point to 51% Gd/Exc). US export sales were weak for old crop, but better than expected for new crop, and US soybean meal exports were reported at a record for the month of May.

Meanwhile, preliminary data for Brazilian June exports pegged showed a record 13.9 mln mt exports (compared to 10 mln mt last year), and 15 cargoes of soybeans were reportedly sold to China. However, newscasts reporting a further contraction in the Chinese sow herd, down 1.68% in June compared to May, do not bode well for overall forward demand.

Palm oil was a little weaker ahead of the MPOB (Malaysian Palm Oil Board) data due on today. Malaysian palm oil exports are expected to have improved, but not enough to prevent an expected 11% increase in stocks compared to May.

Market outlook

US crop condition updates and Malaysian palm oil statistics will be the market focus early in the week, then shift to the USDA-WASDE reports on Wednesday. Analysts are said to be looking for a 246 mln bu loss in new crop soybean production in this week’s WASDE report, with a range of estimates from a 199 mln bu cut to a 376 mln bu cut. Carryout estimates range from 205 to 270 mln bu for old crop and from 128 to 280 mln bu for new crop.

The US soybean balance sheet will be scrutinized intensely and debated for weeks to come. We do not expect any major changes in the WASDE report. But USDA could move to reduce US exports.

Canola Market

Canola usage

The Canadian Grain Commission reported that during week 48 of the crop year, growers delivered 325 thousand MT of canola into primary elevators, exports were an improved 141k MT, while the domestic disappearance amounted to 175 thousand MT.

YTD canola disappearance into week 48 of the crop year is 25% above last year’s (drought-reduced) usage (+3.4 million MT) and amounted to 17 million MT compared to 13.5 million MT last year.

Visible stocks were at 951k MT, with 538 thousand MT in primary elevators, 180 thousand MT in process elevators, 180 thousand MT in Vancouver/ Prince Rupert, and 54 thousand MT in eastern ports.

Current market situation

Crush margins in Canada continued to be quite good, and crushers were paying the best prices to attract seed. We may have to reduce exports a little in our balance sheet, which we think represents a lack of demand rather than a lack of available seed. In the coming season, we will need China to be a big buyer to compensate for the loss in market share to Europe.

We think that StatsCan is too low in their carry-in estimate for 2022/23 by at least 600,000 mt. However, ICE canola remains strong as crop conditions are deteriorating. Both SK Ag and AB Ag did not update their crop assessments last week, but there has been a steady decline in soil moisture. In Saskatchewan, cropland moisture rated as having “adequate” soil moisture fell by 11% from last week to 42%. Similarly, the canola crop ratings fell by 11% from June 12th to 66% Gd/Exc on June 26th. Reports from central Alberta are also not encouraging. It is becoming questionable if average yields will be achieved unless widespread rains alleviate drought stress.

In Europe, Matif rapeseed traded lower last week as harvest is progressing across France. However, this Monday Matif gained €10-11/mt; early harvest reports talk about small seeds and disappointing yields, but final findings can still differ significantly. Increasingly low water levels in the Danube the Rhine also have the potential to upset EU crush and biodiesel logistics.

Market outlook

The USDA soybean balance sheet will be scrutinized closely as will be Canadian crop conditions and crop ratings. Exporters and crushers will be keen to see good yields in Canada to match increased crush and export capacity.

Action

We don’t see the need to make more sales for now.

Canola – Topics of Interest

Sunflower seed production to hit record levels

The International Grains Council (IGC) projects a global sunflower seed harvest of 56.9 mln mt in 2023/24. This would not only be up around 5% on the previous year, but also 1.6 million mt more than previously expected. In other words, the previous record high of 56.2 million mt reached in the 2021/22 season will probably be exceeded by 700k mt. The main reason for the upward revision is expected larger harvests in the EU-27 and Ukraine. Recent favourable growing conditions in parts of the EU are seen to have enhanced yield potential considerably. With 10.5 million mt currently forecast, the EU harvest is likely to be just about 15% larger than the previous year.

The sunflower seed area in Ukraine amounts to 5.3 million hectares. Considering potential land in embattled areas, the IGC estimates the production area at 6.5 million hectares, which would be an 8% increase on the previous year. Harvest is currently estimated at 15.3 million mt, up by ~9 per cent. Russian production in the marketing season 2023/24 is seen to peak at 16.4 million mt for the second consecutive year. In other words, the country is set to remain the world's number one supplier of sunflower seed.

German oil mills sell more rapeseed oil

According to the German Federal Office for Agriculture and Food (BLE), German oil mills sold around 583,800 mt of rapeseed oil to the retail sector and commercial bottlers from July to April of the current crop year 2022/23. This was a 7% increase on the 2021/22 reference period and up 11% on 2020/21. In the same period, 202,200 mt of rapeseed oil went to the food industry, down 2% on the reference period.

However, foreign trade in rapeseed oil from oil mills in Germany rose 13% to 303,800 mt compared to the same period a year earlier and as much as 29% compared to 2020/21.

Rapeseed oil sales reached around 108,200 mt in April 2023, after peaking at 121,100 mt in March 2023.