Canola Market Outlook: December 11, 2023

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans: CBOT Jan soybeans had a huge 31 ¾ cent range on the day and finished out the week with a net 21 cent loss. Jan. soybean meal futures ended down by $8 for the week. Soybean oil futures traded lower with the Jan. contract weekly loss at 125 points.

In their report, USDA left the US balance sheet unchanged with the average soybean cash price at $12.90/bu. Meal was $10/mt higher at $390 and soybean oil 4 cents weaker at 57 c/lb.

USDA raised Brazil’s 2023 crop by 2 mln mt to 160 mln mt, in-line with expectations. World ending stocks are lowered (-229k mt globally; -2.3 mln mt excl. China) mostly due to lower Brazilian stocks. – We saw nothing bullish in the report.

Chinese import demand and US biodiesel disappearances will remain the key demand variables.

Canola: YTD canola disappearance into week 18 of the crop year amounts to 5.9 million MT compared to 6.3 million MT last year and is down 7% on last year.

STC’s canola production numbers were an astonishing 5.5% (or +960k mt) higher than in their September report. Note the USDA subsequently raised canola production to 18.8 mln mt!

USDA raised global ‘23/24 canola production to 87 mln mt, 2% smaller than last year’s global canola production, but USDA forecasts the ‘23/24 global rapeseed trade at 17.1 mln mt, which is 15% (-3.1 mln mt) smaller than last year’s rapeseed trade.

Overall, Chinese demand remains a key variable to oilseed markets and while soybean oil has its bull story in US biofuel demand, world vegetable oils currently lack a driver.

Assuming you are 80% sold, we would leave canola sales alone for now.

Oilseed Market Backdrop

Soybeans

Current market situation

CBOT soybeans settled with prices 4 to 7 ¾ cents in the red on Friday. The Jan contract spiked below $13/bu following the USDA report but closed at $13.04/bu. Jan soybeans had a huge 31 ¾ cent range on the day and finished out the week with a net 21 cent loss. Jan. soybean meal futures ended down by $8 for the week. Soybean oil futures traded lower with the Jan. contract weekly loss at 125 points.

In their report, USDA left the US balance sheet unchanged with the average soybean cash price at $12.90/bu. Meal was $10/mt higher at $390 and soybean oil 4 cents weaker at 57 c/lb. USDA raised Brazil’s 2023 crop by 2 mln mt to 160 mln mt, in-line with expectations. Elsewhere, Canadian canola production was raised 1 mln mt to 18.8 mln mt and Australian production was raised 0.4 mln mt to 5.5 mln mt. There were no changes to US soybean oil or Chinese domestic demand, although Chinese imports were raised 1mln mt for ‘23/24 to 102 mln mt. World ending stocks are lowered (-229k mt globally; -2.3 mln mt excl. China) mostly due to lower Brazilian stocks. – We saw nothing bullish in the report.

In S America, Brazil plantings reached 83% complete whilst Argentine plantings are 52% complete. BAGE kept the crop at 50 mln mt versus the USDA 48 mln mt.

Market outlook

Soybean sales are still 16% below last year’s, (USDA down 12%), and crude oil fell to 5-month lows in the background.

Chinese import demand and US biodiesel disappearances will remain the key demand variables.

Canola Market

Canola usage

The Canadian Grain Commission reported that during week 18 of the crop year, growers delivered 352 thousand MT of canola into primary elevators, exports were a somewhat improved 133 thousand MT, while the domestic disappearance showed 238 thousand MT.

YTD canola disappearance into week 18 of the crop year amounts to 5.9 million MT compared to 6.3 million MT last year and is down 7% on last year.

Visible stocks were shown at 1.17 million MT, with 630 thousand MT in primary elevators, 196 thousand MT in process elevators, 173 thousand MT in Vancouver/ Prince Rupert, and 167 thousand MT in eastern ports.

Current market situation

Statistics Canada (STC) issued their ‘final’ 2024 crop production estimates on Dec. 4th. At an estimated 18.328 mln mt, STC’s canola production numbers were an astonishing 5.5% (or +960k mt) higher than in their September report. This still leaves the 2023 production 2% smaller than last year’s, mostly due to a reduction in acres. (Note the USDA consequently raised canola production to 18.8 mln mt!)

It seems that the trade was also expecting the higher production number with an average pre-report estimate at 18.3 mln mt. However, the range in estimates was a huge 2.5 mln mt (17.2 to 19.7 mln mt), so there still seems to be no general agreement on the size of this year’s canola crop. But the market reacted negatively to the news of a bigger crop against very tepid export demand for canola. We note that ABARES in Australia also increased their ’23 canola crop estimates by 372k mt to 5.523 mln mt [see detail below].

Pls note that the December STC number is much closer to the Mercantile numbers than their previous one.

The combined STC-ABARES changes add to roughly a 1.4 mln mt increase in global canola production this year to 87 mln mt (USDA number). This is 2% smaller than last year’s global canola production, but USDA forecasts the ‘23/24 global rapeseed trade at 17.1 mln mt, which is 15% (-3.1 mln mt) smaller than last year’s rapeseed trade.

Market outlook

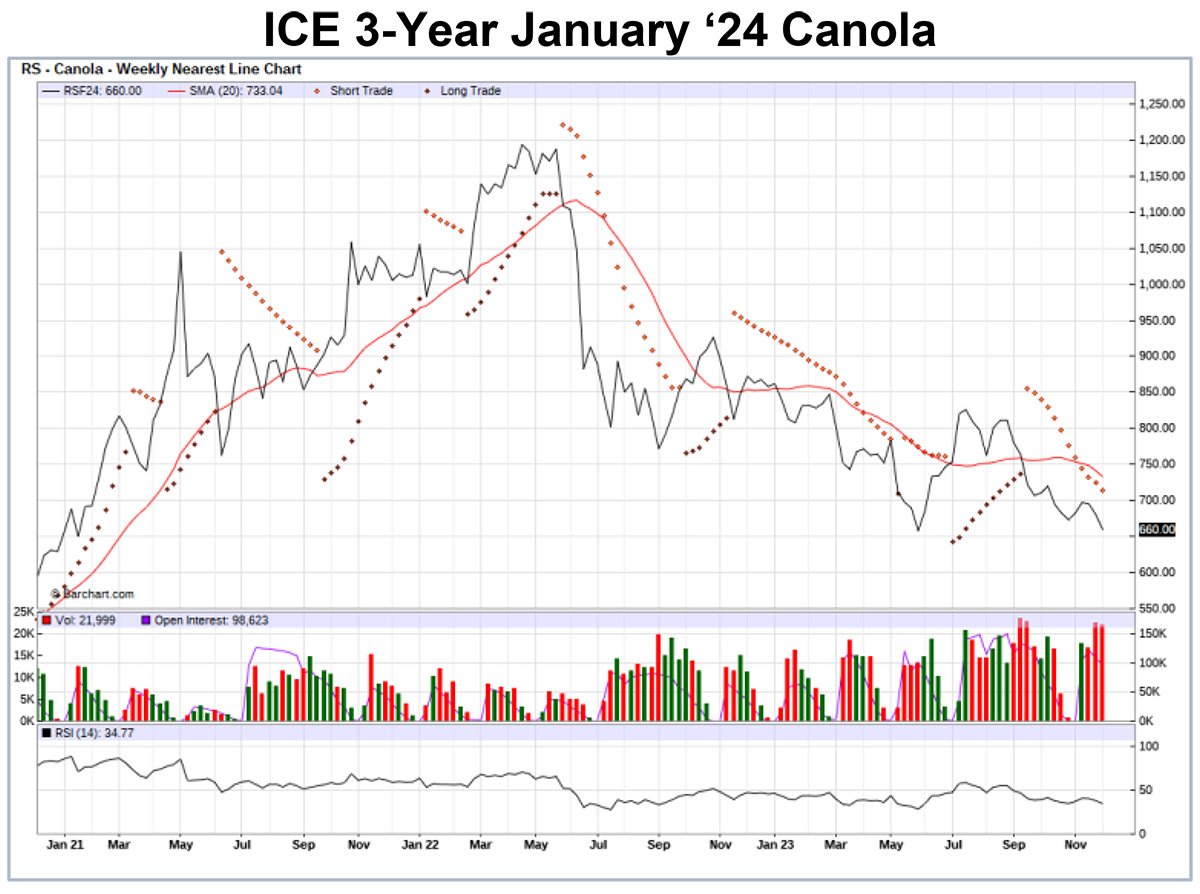

Canola is following soybean oil (up and down), and the fate of the two markets are inter-twined with the US biodiesel industry and sentiment. Rapeseed in Europe lagged, as its fate is more closely tied to world vegetable oil prices.

Overall, Chinese demand remains a key variable to oilseed markets and while soybean oil has its bull story in the US due to biofuel demand, world vegetable oils currently lacks a driver.

Action

Assuming you are 80% sold, we would leave canola sales alone for now.

Canola – Topics of Interest

Statistics Canada: December production numbers

ABARES: Australian canola crop estimates

According to estimates released by ABARES in its December 2023 Australian Crop Report, Australia is forecast to produce 5.5 mln mt of canola. Compared with estimates released in their September report, canola production is up 7.2%. The increase from September reflects improved prospects in southern cropping regions, which are expected to more than offset reduced production in parts of New South Wales, Queensland and Western Australia.

However, while the Australian canola acreage this year was down by 11% (-414k ha), the ‘23/24 Australian canola production is down by 33% (-2.57 mln mt) from the record ‘22/23 production.

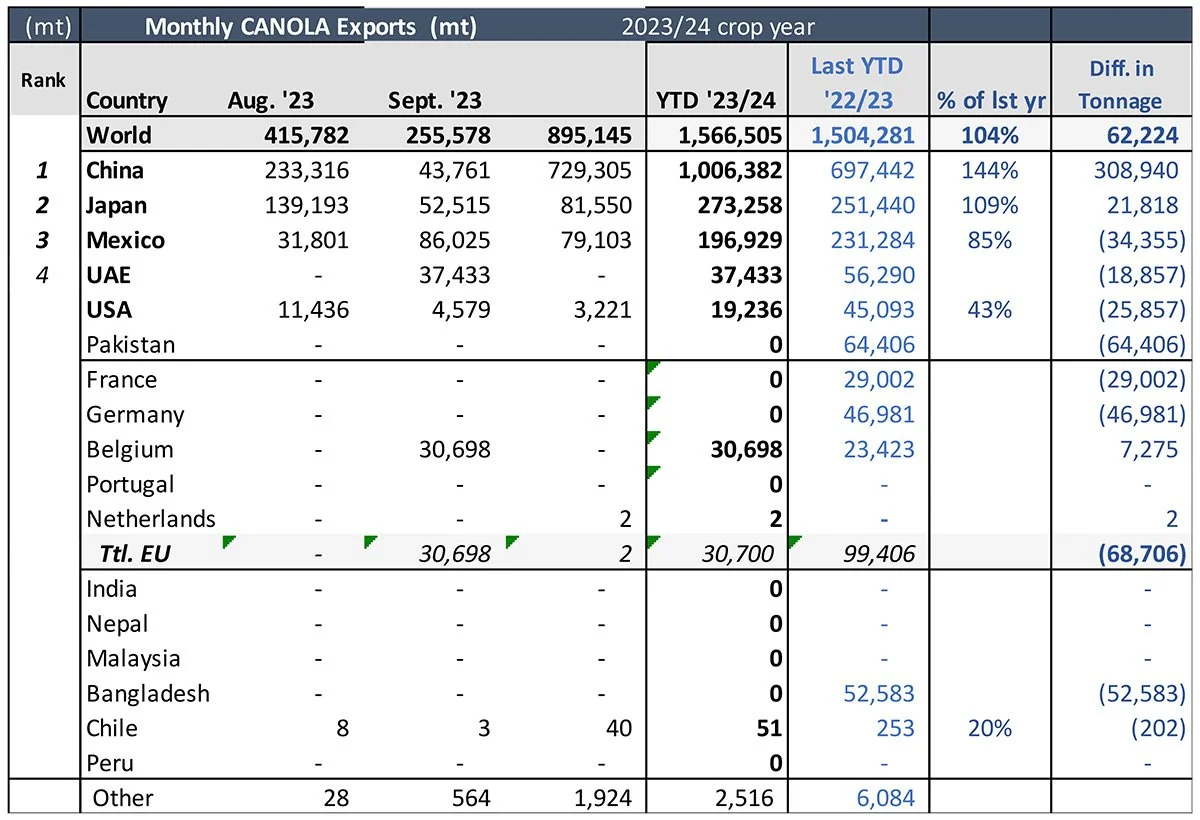

StatsCan: Cdn. October canola exports by destination:

Canada exported 895k mt of canola during October 2013. 64% of the monthly total (729k mt) went to China, and 9% each (82 and 79k mt) went to Japan and to Mexico.

Year to date exports (Aug. through to the end of Oct.) total 1.566 mln mt, compared to 1.5 mln mt last year to date.