Canola Market Outlook: August 26, 2024

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans: The CBOT soybean complex was firm, posting 8 ¼ to 11 ½ c/bu gains across the board.

New crop sales were well above trade guesses; weekly total flash sales to all destinations added to 1.384 million MT for the week.

ProFarmer pegged soybean yield at 54.9 bu/ac and production at 4.74 bln bu. That is bigger than the current USDA numbers at 53.2 bu/ac and 4.589 bln bu.

There are hints of markets finding lows as S American product premiums continue to be well supported. We think the soybean/corn spread will stop narrowing while there is soybean export demand.

Canola: YTD total canola disappearance into week 2 of the crop year amounts to 1.14 million MT compared to 629 thousand MT last year and is up 81% on last year.

Very little canola has been harvested. The production outcome of Cdn. canola still needs watching.

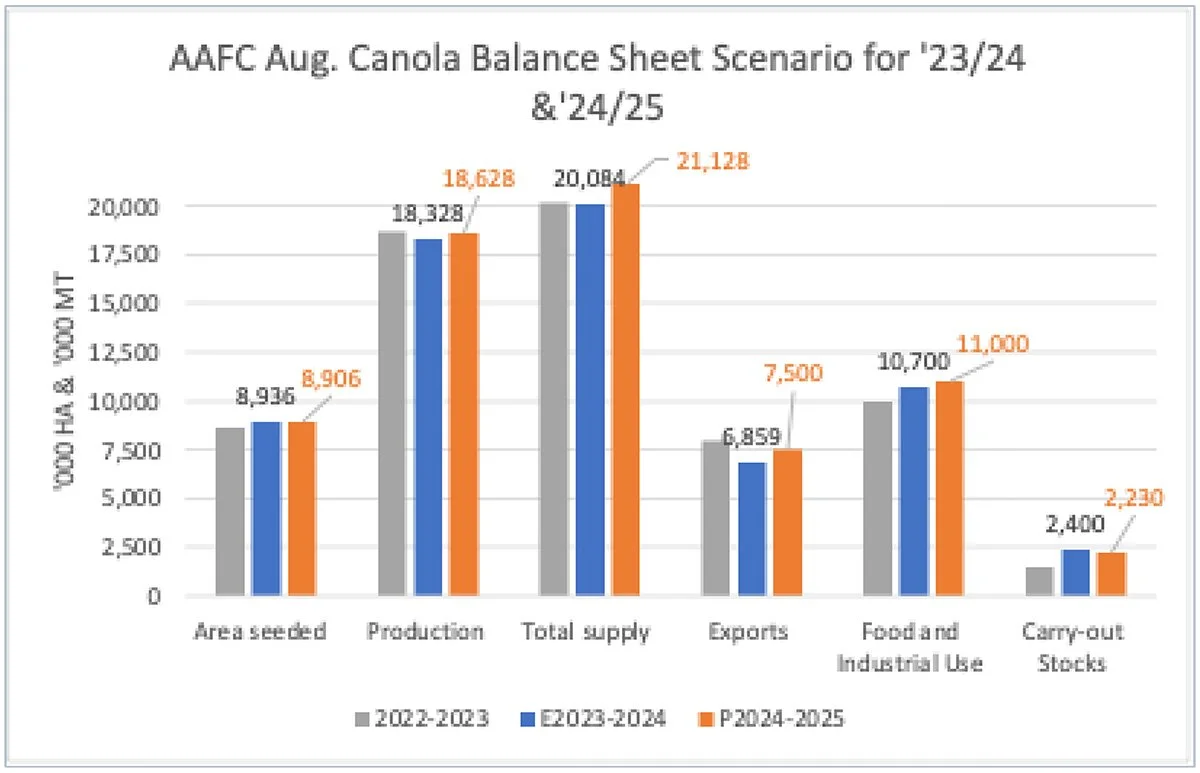

In their August canola balance sheet, AAFC increased both ‘23/24 and ‘24/25 canola ending stocks.

Crush margins are ruling the bids to growers at present.

While oil prices are stronger, we would hold additional sales for now.

Oilseed Market Backdrop

Soybeans

Current market situation

The CBOT soybean complex was firm, posting 8 ¼ to 11 ½ c/bu gains across the board. Soybean meal futures were mixed on the session, from 40 cents higher to down $1.30 per ton. Soy Oil rallied to end the week with gains of 97 to 140 points.

CFTC data showed that large managed money spec funds in soybean futures and options added back 8k Ct’s to their net short position, to a near record 182,758 contracts. Commercials added to their net long position, not at a record 87,940 contracts as of August 20.

New crop sales were well above trade guesses; weekly total flash sales to all destinations added to 1.384 million MT for the week.

Following their 4-day crop tour, ProFarmer released projections for the US soybean crop after the close. They pegged soybean yield at 54.9 bu/ac and production at 4.74 bln bu. That is bigger than the current USDA numbers at 53.2 bu/ac and 4.589 bln bu.

Brazilian premiums stayed very firm, with spot around +140Nov +250Nov for Sept/Oct (PNW was done at +230 Nov, while Nov Gulf traded at +240Nov.) Vegetable oils are slowly building an upward trajectory away from last week’s lows, but Bursa Palm Oil remains locked in a tight trading range.

Market outlook

Futures and premiums are firming as the market takes account of the extended price declines and the improved demand outlook, while harvest looms. There are hints elsewhere of markets finding lows as S American product premiums continue to be well supported.

We think the soybean/corn spread will stop narrowing while there is soybean export demand.

Canola Market

Canola usage

In week 2 of the crop year, growers delivered 320 thousand MT of canola into primary elevators, exports were a decent 278 thousand MT, while domestic disappearance amounted to 199 thousand MT.

YTD total canola disappearance into week 2 of the crop year amounts to 1.14 million MT compared to 629 thousand MT last year and is up 81% on last year.

Visible stocks fell to 1.5 million MT, with 875k MT in primary elevators, 196 thousand MT in process elevators, 226 thousand MT in Vancouver/ Prince Rupert, and 198 thousand MT in eastern ports.

Current market situation

There were more farm stocks left at the end of last crop year than we thought, so we will have to adjust either acres or yield for the ’23/24 crop balance sheet. We will wait into week 4 of the new crop year before we adjust our estimate.

Regarding harvest, SK Ag reported only 2% of canola harvested as of Aug. 19th, AB Ag showed 0.2% harvested, and MB Ag zero percent. So, it remains to be seen if and how the hot temperatures in July and August affected this year’s yields.

AAFC came out with their August canola balance sheet last week. AAFC made some significant changes to their ‘23/24 canola S & D. They reduced ‘23/24 canola exports by 141k MT to 6.859 million MT and lowered feed/waste dockage by a big 509k MT to 74k MT (?). This then increased ’23/24 ending stocks from previously 1.75 million MT to 2.4 million MT. For the ’24.25 crop year, AAFC left yields and production unchanged at 2.12 MT/ha and 18.63 million MT respectively, but the higher carry-in increased ‘24/25 ending stocks to 2.23 million MT, despite their increase of exports from 7 to 7.5 million MT.

Canola markets were fairly stable leading into the harvest and into the rail strike. On Saturday, the Canada Industrial Relations Board ordered a halt to the work stoppages at railways, signaling an end to the unprecedented service disruption at both main freight rail companies. However, according to the railways, it will take weeks to unroll all the implications of working up to the stoppage. Nov. canola closed up by $4.90/MT on Monday, Matif rapeseed was up by €5.25.

In Europe, Matif rapeseed continued its choppy price action, with weak bio-diesel demand pressuring rapeseed oil values. But low water levels in the rivers Rhine and Danube are pressuring logistics and spreads, with the Nov-Feb carry widening back out to €4.

Crush margins are ruling the bids to growers at present.

Market outlook

Vegoil’s are slowly building an upward trajectory away from last week’s lows, although palm oil remains locked in a tight trading range. Futures and premiums are firming as the market takes account of the extended price declines and the improved demand outlook vis-à-vis the looming harvest.

The yield/ production outcome of Cdn. canola still needs watching.

Action

While oil prices are stronger, we would hold additional sales for now.

Canola – Topics of Interest

USDA – Global vegetable oil production continues to grow

According to USDA, global production of vegetable oils is growing, as is demand. Especially palm and soybean oil are likely to be significantly more abundant in 2024/25, more than offsetting the decline in sunflower oil.

USDA expects global production of vegetable oils in the current crop year to hit a record level at 224.2 million MT, a 2.7 million MT rise year-on-year. Consumption is estimated at 221.7 million MT, up 5.3 million MT on the previous year. Ending stocks are poised be lower than the previous year at 29.6 million MT and also fall short of the long-standing average.

Palm oil production is set to reach yet another record volume in 2024/25, up 0.8 million MTs on the 2023/24 output.

Given the ample supply of feedstock, supply of soybean oil is likely to grow just less than 3.2 million MT, hitting a new record at 65.5 million MT.

Production of rapeseed oil is also set to reach a record level at 34.2 million MT.

But the USDA expects sunflower oil production to plummet in 2024/25, especially due to a more than 1 million MT decline in production in Ukraine. The world forecast was lowered almost 1 million MT month-on-month to 20.6 million MT, sliding just under 2 million MT below the previous year's volume. This would be the lowest output since 2021/22.