Canola Market Outlook: April 10, 2023

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans – After an initially good start to the week, CBOT soybeans closed the week last Thursday with a 13 cent weekly loss for the May contract, and a 10 cent weekly loss for the November contract.

US weekly soybean sales reached 155 thousand MT, down 56% from the preceding week. Sales also were below expectations of ~200k mt. Cumulative sales are at 91% of the March WASDE projection.

Our bias is bearish, and we think the ratio to corn is too high.

Canola – YTD canola disappearance into week 35 of the crop year is 26% above last year’s (drought-reduced) usage (+2.7 million MT) and amounted to 13 million MT compared to 10.3 million MT last year.

Both Matif rapeseed and ICE canola futures ended the week lower after solid gains earlier in the week.

We expect that the oil value in the crush will keep China buying canola seed and we expect Mexico and Japan to take their normal quantities at current prices.

The carry-over is mostly in farmers’ hands, but old crop is underpriced at present. New crop canola is still a whole season away. We would not sell old crop or new crop right now.

Oilseed Market Backdrop

Soybeans

Current market situation:

Last week started well for CBOT soybeans after supportive stock and acreage data last Friday. But weakness accelerated through the latter part of the week: CBOT soybeans closed down for the week last Thursday (ahead of the Easter weekend) with 5-18 cent losses, which translated into a 13 cent loss over the week for the May contract, and a 10 cent weekly loss for the November contract. Soybean oil was down 96 points for May.

However, the Commitment of Traders report last Friday showed managed money spec funds comfortably in the bull camp as of April 4, with a net long of 146 thousand contracts. Funds added 31 thousand longs and shed 15 thousand shorts during the week.

US weekly soybean sales reached 155 thousand MT, down 56% from the preceding week. Sales also were below expectations of ~200 thousand MT. Cumulative sales are at 91% of the March WASDE projection.

We are expecting the next WASDE report on Tuesday, and analysts generally expect an 11 mln bu tighter carry-out, which would drop stocks below 200 mln bu. For Argentina, a 29.2 million MT crop is expected to be published in the report. This would be 3.8 million MT smaller than in the March WASDE report.

BAGE in Argentina estimated their soybean crop at 25 million MT, the same as their previous estimate. The USDA Ag Attaché estimated the 2023/24 Paraguayan soybean crop at 10 million MT, up from 8.8 million MT in 2022/23. Safras and Mercado in Brazil reported the Brazilian 2022/23 soy harvest 80.8% complete, down from 85.5% last year.

As mentioned last week, Argentina has a new soy-peso, where exporters receive 300 pesos for every dollar, which is 72 pesos more than the price set by the government. Brazilian premiums continue lower and US markets are taking stock of weak sales and begin to wonder whether weaker sales are a hint of things to come.

Market outlook:

The old crop soybean-corn ratio was 2.28 and the new crop 2.38, so we will leave them alone for the time being.

The US weather market is upon us with high acreage and yield ideas expressed by the USDA that will be difficult to reach. We will leave this market alone for the present. However, our bias is bearish, and we think the ratio to corn is too high.

Canola Market

Canola usage:

The Canadian Grain Commission reported that during week 35 of the crop year, growers delivered 399 thousand MT of canola into primary elevators, exports were at 147 thousand MT, while the domestic disappearance amounted to 216 thousand MT.

YTD canola disappearance into week 35 of the crop year is 26% above last year’s (drought-reduced) usage (+2.7 million MT) and amounted to 13 million MT compared to 10.3 million MT last year.

Visible stocks were at 1.16 million MT, with 679 thousand MT in primary elevators, 243 thousand MT in process elevators, 130 thousand MT in Vancouver/ Prince Rupert, and 106 thousand MT in eastern ports.

Current market situation:

Matif rapeseed and ICE canola futures ended the week lower after solid gains earlier in the week. However, while it took a week to get Matif up from €420/mt to €490/mt, it took 2 days to undo half of the gains. EU sunflower seed imports have fallen to around half the pace of the first two quarters of the season, but rapeseed imports remain strong, with Ukrainian and Australian canola sales to the EU up by ~80% while Canadian exports to the EU are down 62%.

However, we expect that the oil value in the crush will keep China buying canola seed and we expect Mexico and Japan to take their normal quantities at current prices. Canadian YTD canola exports to China are up by 1.6 million MT over last years (2.8 fold); we expect exports to Japan to speed up over the next quarter (currently down 34% from last years); and YTD exports to Mexico are on par with last years.

Regarding new crop, Canadian traders are somewhat worried about planting conditions with heavy snow melt from the northern US expected to bring spring flooding along the Red River. Asian vegetable oils were all higher.

Market outlook:

Oilseed markets have become quite complex: we are expecting adjusted tighter US soybean ending stocks and a smaller Argentine crop in the April WASDE report. Meanwhile, EU oilseeds look weak, and the Brazilian soybean basis is collapsing while the US soybean basis is strong. Crush margins have been deteriorating.

For Canadian farmers, export values should be better than the domestic crush and we think G3 is likely the best bidder.

Action:

The carry-over is mostly in farmers’ hands, but old crop is underpriced at present. New crop canola is still a whole season away. We would not sell old crop or new crop right now.

Canola – Topics of Interest

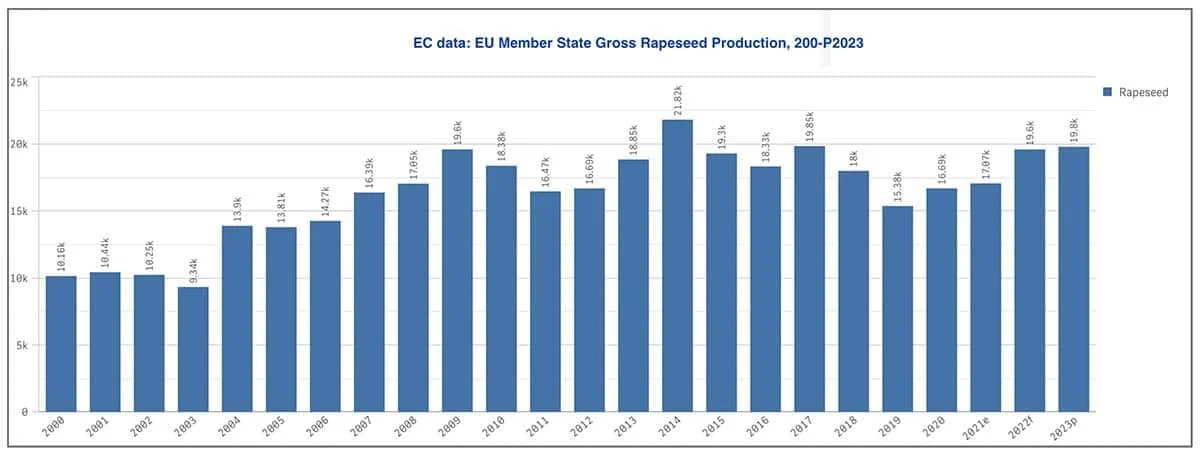

European Commission (EC) data on Rapeseed Production

According to the EC, European Union rapeseed production by all member states is expected to reach 19.8 million MT this year, about the same as was achieved in 2017. If this proves correct, it would be the second highest annual production, only lagging 2014, which yielded 21.8 million MT.