Canola Market Outlook: November 13, 2023

Weekly canola market outlook provided by Marlene Boersch of Mercantile Consulting Venture Inc.

Key Points for the Week

Soybeans: January soybeans spiked to over $13.80/bu, as the market continues to worry about weather conditions in Brazil and takes stock of large Chinese purchases.

The USDA report last Thursday showed US ending stocks 25 million bu higher than in the October report at 245 million bu due to a yield increase to 49.9 bu/acre.

However, the trade is getting increasingly concerned about growing and planting conditions in Brazil while there is little change in forecasts.

Canola: The USDA-WASDE showed no significant changes to the EU, Australian or Canadian rapeseed production and crush outlooks, but the Ukrainian sunflower seed crop was raised by 500k MT to 14.5 million MT and is now 2.3 million MT higher than last year’s.

We need to see bigger Canadian exports, otherwise we will end up with a burdensome carryover.

We would be sold up to 80 percent of canola production.

Oilseed Market Backdrop

Soybeans

Current market situation

January soybeans spiked to over $13.80/bu, as the market continues to worry about weather conditions in Brazil and takes stock of large Chinese purchases. Brazil is still too in the wet in the South, and too dry in the North. Brazilian soybean plantings are around 61% complete, against 73% last year and 70% on average. Argentine weather looks better, but old crop supplies are gone.

The USDA report last Thursday showed US ending stocks 25 million bushel higher than in the October report at 245 million bushel due to a yield increase to 49.9 bu/acre. The market turned lower, but products were not as weak, which pushed crush margins higher. In the WASDE report, the Chinese soybean crush was raised 1 million MT for both old and new crop, but the old crop imports were lowered by 1.1 million MT to 100.9 million MT, while new crop imports were left unchanged at 100 million MT. Chinese ending stocks were shown down 3.5 million MT, non-Chinese stocks up 2.4 million MT, essentially due to the hike in Brazil's 2023 crop number to 158 million MT (+2 million MT).

There were no notable changes to Asian palm oil balance sheets. However, the Malaysian Palm Oil Board (MPOB) showed an almost 6% increase in stocks to 2.45 million MT, a 4-season high, although slightly below the trade estimate of 2.56 million MT.

Market outlook

The global oilseed production forecast was raised by 2 million mt this month to 661 million mt on larger Russia rapeseed and soybean, Ukrainian soybean and sunflower seed, and U.S. soybean crops.

The 245 million bu carryout in US soybeans is not really bullish, but the trade is getting increasingly concerned about growing and planting conditions in Brazil while there is little change in forecasts. These are prices that ration soybean meal demand and funds are at or near record long.

Canola Market

Canola usage

The Canadian Grain Commission reported that during week 14 of the crop year, growers delivered 292 thousand MT of canola into primary elevators, exports were at a small 68 thousand MT, while the domestic disappearance showed 189 thousand MT.

YTD canola disappearance into week 14 of the crop year amounts to 4.5 million MT compared to 4.4 million MT last year and is up 3% on last year.

Visible stocks were shown at 1.1 million MT, with 565 thousand MT in primary elevators, 184 thousand MT in process elevators, 200 thousand MT in Vancouver/ Prince Rupert, and 146 thousand MT in eastern ports.

Current market situation

Rapeseed and canola ended the week with a mixed performance, but with canola starting to gain on rapeseed. However, EU oilseed imports are down 24% compared to last year.

The USDA-WASDE showed no significant changes to the EU, Australian or Canadian rapeseed production and crush outlooks, but the Ukraine and Russia both show increased crush with Russian production increased by 500k MT to 4 million MT, close to last year’s record level. The Ukrainian sunflower seed crop was raised by 500k MT to 14.5 million MT and is now 2.3 million MT higher than last year’s.

We really need to be seeing bigger Canadian exports, otherwise we will end up with a burdensome carryover. YTD exports only adds to 6.13 million MT for the year, which would fall short our expectation by almost 1.9 million MT.

Crush margins remain very good. YTD crush numbers prorate to 10.53 million MT, 530k MT higher than expected, but this still would not be enough to compensate for a small export program.

Market outlook

If Canadian canola exports do not improve, we will need to reduce our export forecast of 8 million MT, which would increase ending stocks.

Action

We would be sold up to 80 percent of canola production.

Canola – Topics of Interest

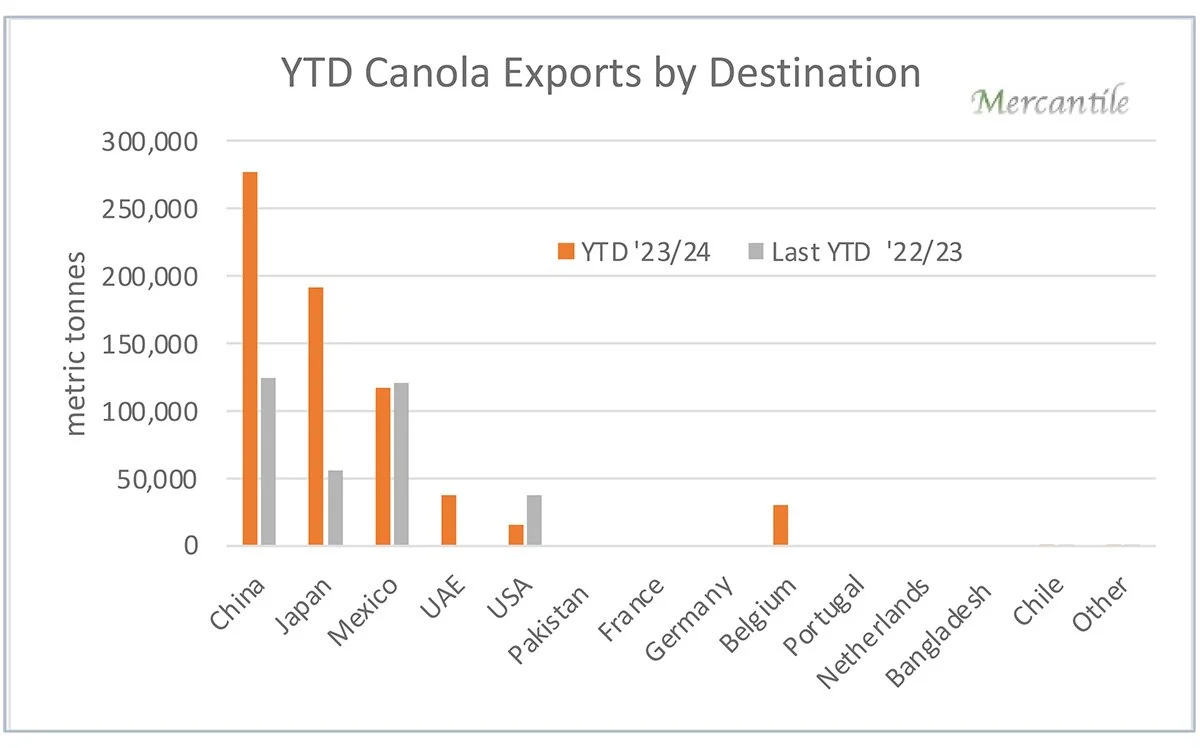

Statistics Canada: Canadian September Exports by Destination

According to StatsCan, September canola exports reached 256k MT, compared to 280k MT last crop year. Year-to-date (Aug.-Sept.) exports added to 671k MT due to good export volumes in August this year.

Worryingly, China dropped off as the most important destination, ranking behind Mexico and Japan in September. We note that one cargo of canola went to the EU (Belgium) during the month.

USDA: Global Canola Production

USDA is pegging global canola production for 2023/24 at 85.6 million MT, down 4% from 88.8 million MT last crop year. The EU remains the biggest rapeseed producer at 20.1 million MT, followed by Canada (17.8 million MT), and by China (15.4 million MT).

However, USDA also estimated imports down by a big 21% from 20 million MT in ‘22/23 to 15.8 million MT in ‘23/24. The reduction in expected imports is due to smaller purchases by China (-1.9 million MT) and by the EU (-1.7 million MT). Rapeseed ending stocks are expected at 6.5 million MT, down from 7.8 million MT last crop year.